Nice edit

Speaking of edits - no-one reading this in 30 mins+ will have a clue about what on earth happened in this thread!

Nice edit

Speaking of edits - no-one reading this in 30 mins+ will have a clue about what on earth happened in this thread!

Oh wow ![]()

Please quickly lock the topic and put an end to all of this before people pick holes in it and drag it on even longer than it already has ![]()

The big announcement about Cheque Imaging is going to be a bit of an anti-climax when it arrives.

Nooooo…

Don’t lock it - this happily sees off another request from the early days and we’re all so happy to see the request for Cheque Imaging getting a ![]() against it

against it ![]()

What’s next?

Something easy, obvs.

Joint account parity

I’ll see myself out

If you ignore the #1 request (Plus/Premium for Joint accounts - 524 votes), which has recently been internally brushed aside, we’re now anywhere between wanting a Web version access for the Monzo app (353 votes) and 'Merchant Grouping’ (0 votes)

Not live for me either. Though I think i’ve only had a cheque once in my entire life

Must be rolling out slowly, I had it on iOS from last night.

I might have mentioned this in a different thread, but I think its a bad choice by Monzo to place the entry point to this “other ways to add money” screen at the bottom of a list of banks which can be used for open banking transfer. Its very hidden in this location (and also the open banking transfer list lacks a bit of context). IMO it would be much better if this “other ways to add money” screen is the first screen you see after you tap “add money”, with “open banking transfer” added as an option on this screen.

Agreed. Bank transfer, except when initially joining Monzo, is my least-used method of adding money because pretty much everything I have is in Monzo. Except stuff that comes from other people.

I wholeheartedly agree.

The strange prominence of Open Banking transfer supports the widespread misconception that Monzo is “not a real Bank” and a “top-up” led prepaid card. This is not helpful to customers or Monzo itself.

On the face of it, yes.

In actuality, neobanks have been somewhat slow to roll this out (due to a reluctance to deal with cheques at all) whereas traditional banks have jumped on it as a chance to justify branch closures. So the incentive is probably weighted more heavily in favour of high limits for the traditional banks, as the alternative is arguably to pay in a cheque at a branch which they no longer want customers to be doing. Neobanks probably think the alternative is not to have to deal with cheques, as customers with accounts elsewhere (with traditional banks) would probably just use their other account instead.

I don’t have this option yet. Still the old format of posting it which can take 1-2 weeks.

Me too, on iOS.

I wonder how long the phased rollout will take?

me neither. I’m putting it down to living in rural dorset.

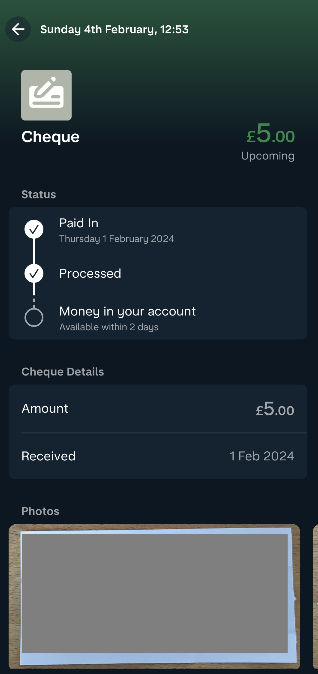

Decided to write myself a cheque and pay it in. Didn’t take screenshots, but process was straightforward: app guides you through taking a photo of front and back, then asks you to enter the amount and an optional reference. Then you submit and you see a confirmation screen telling you to allow “up to 3 business days for the money to appear in your account” and reminding you to hold onto the cheque in the meantime in case of any issues. An upcoming payment (dated/categorised “3 days from now”) also appears in your feed.

Does the image of the cheque become an attachment to the paying-in money transaction? It does with Starling.

The transaction entry in the feed has a photos section showing you the photos you took. I’ll take another look in a couple of days to see if the photos are still there when the cheque has cleared.

Hopefully they are, otherwise it can be hard to work out who a payment was from when it’s a credited cheque (assuming that the reference doesn’t make it clear) looking back later.

Even worse, if you pay in cheques at a branch or Post Office with traditional banks, you get no reference showing at all.

In relation to this - there was an option to specify a reference whilst paying in the cheque (i.e. when taking the photos) however neither a reference field nor a notes field is currently present on the transaction screen accessed from the transaction feed. Don’t know if that’s because its still pending or if its because I chose not to supply a reference when I paid in.

Suggestion to Monzo - it would be helpful I think to to show at least a notes field whilst the cheque is pending. I notice notes field is available whilst incoming bacs payments are pending. Would be good to also have for pending cheque deposits.

Edit…

Here’s what the transaction screen looks like whilst waiting for the cheque to clear. I’ve masked the portion of the screenshot showing the cheque image.