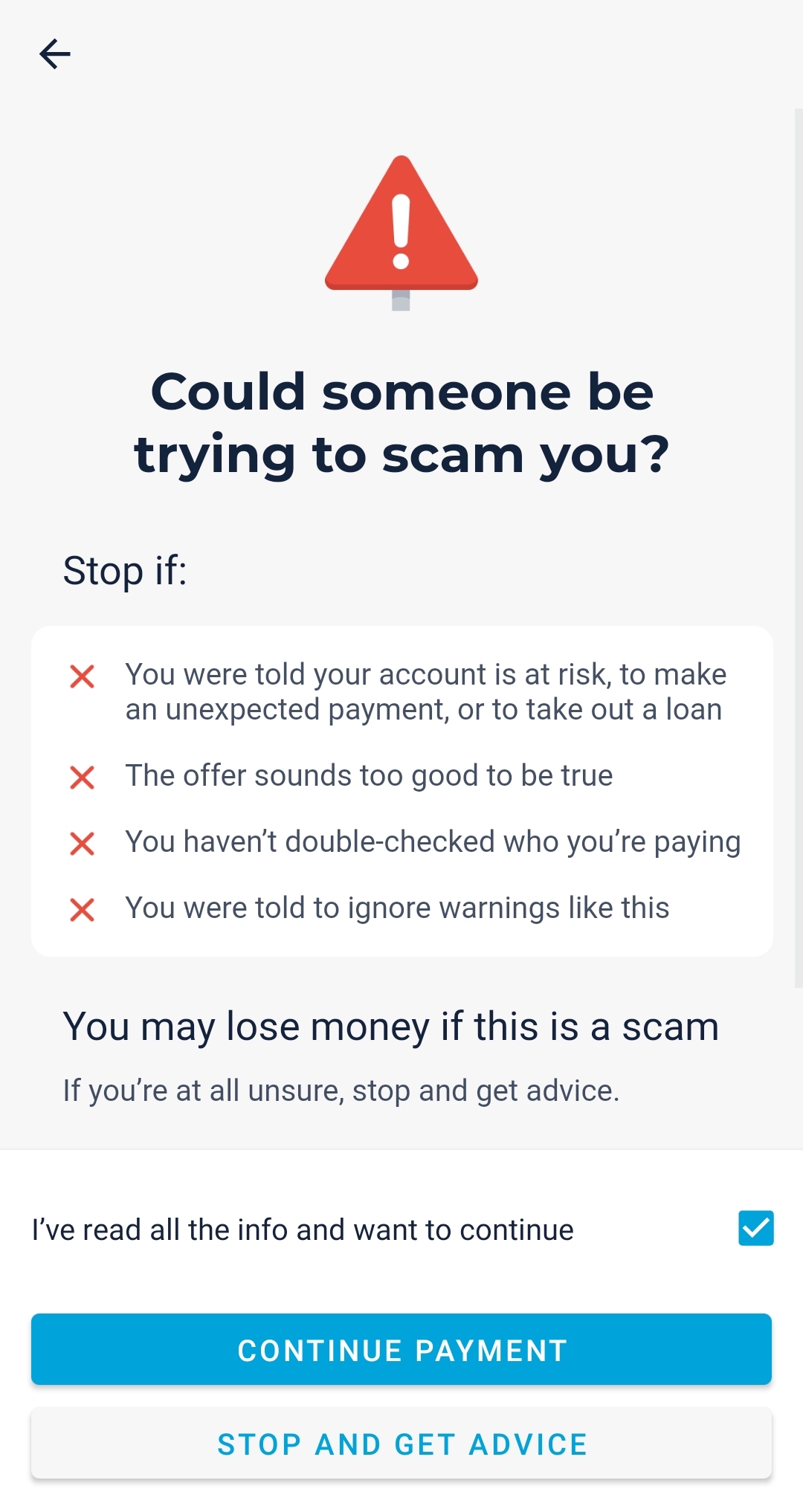

Issue: The app reports Sort code 77-29-00 Bank account 00000000 as unable to verify, could be scam etc. However, it’s the official payment bank account details for paying any MBNA credit card, possibly any Llyods credit card. The reference is your credit card number. Since they’re the entire bank and own the entire sort code, they probably don’t care about the account number.

See screenshot of “How to pay” section of my MBNA credit card statement. Alternatively, call MBNA and ask what their official payment Sortcode and bank account number is. Also see last screenshot of verification from MBNA that they received the payment (I made a small payment first just in case).

Suggest adding this and some other bank account numbers to a white list or something. Ideally would be better if there were built-in support for these types of accounts, that ensure you put your own credit card number in the reference field etc.

Details to reproduce: Attempt to pay Sort code 77-29-00 Bank account 00000000 OS: Android Device: n/a App Version: 3.43.3

I don’t see an issue with how Monzo do it when you first send - even to a credit card (as @TonyHoyle states).

My issue is they still ask you every time, even when I’ve already stated its all good in a previous payment. There should be an ‘I trust this account’ checkbox to stop it annoyingly popping up.

I wish they’d do a onetime verification then only make you go through this check if you make amendments ie set it to remember it’s a credit card payment and only trigger a check if you change the reference .

Admittedly, I’ve had a scheduled/repeating payment from Monzo to MBNA for years set-up, before SCA & increasing fraud protection arrived, but I’ve never had a problem paying the 77-29-00/00000000 with the CC number as the reference - as a recurring scheduled payment.

The ‘warning’ display you’ve shown is likely flagged up when you attempt an initial single payment - there’s nothing wrong, it’s just a reminder to check all is OK before letting the money go.

OTOH a scammer might want you to pay money into that account to give money to someone elses credit card, so the warning seems fair.

By that logic, any transaction for anything could be a scam. A scammer outside a supermarket could convince me to buy them something inside, turns out their not homeless but on 40k/year. Literally every single transaction could be a scam. Even receiving money could be part of a scam - maybe I got scammed on a cash loan service from some thugs.

At some point, common sense must prevail, we can’t be inundated with warnings on every transaction.

I suggest

at the very least, only do this warning once, not every transaction - yes I tested it, it happens EVERY time

longer term, add better support for paying off credit cards generally

It’s 2023, this still happens. I feel like there’s a drop in innovation at Monzo (not just because of this).

If you bank transfer to pay American Express or MBNA, it will go to a generic 00000000 bank account number within those bank’s Sort Code, but the details of the transaction is the credit card number you’re paying off. I guess it’s psuedo account routing via the details/message of the transaction.

For both these, and similar cases, there should be a different message than not trusting the account - the account is fine, it’s all about the transaction details that routes it to an account.

Regardless of the UX treatment, if I’ve approved and sent to the same combination: Sort code + Account + Details/Message before, then I shouldn’t be warned again; but especially for paying off American Express / MBNA / etc if the message (ie the credit card being paid off) is the same.

With both of these providers you can initiate the transfer from their app. You then won’t need to provide any details, worry about typing in the wrong info or be asked if you’re being scammed.

MBNA > Pay Credit Card > From your UK bank account.

AMEX > Make Payment > Pay with bank transfer.

Presumably you’ll be starting the payment process from the credit card app anyway as you’ll be checking your balance first.

That’s an option but, for whatever reason, not everyone will like doing it that way. Many simply just won’t be comfortable with how Open Banking works and also may possibly not want to give out their debit card details to their credit card provider. This is understandable. Having a traditional way to pay off the balance directly is still important - alongside other options such as Direct Debit, Open Banking and debit card. I won’t argue against credit card providers that have decided to scrap the Bank Giro Credit cheque/cash payment option as that is very niche now, but a bank transfer option is important.

Another reason I could think of, just off the top of my head, is if the customer has a low credit limit and they want to pay off some of all of their balance early to allow for more credit card spending whilst staying within the limit. Some providers will not let you use the Open Banking or debit card payment options if you don’t have a statement balance owing - but bank transfer would work. Using specialist credit cards to withdraw cash abroad is another instance where somebody may want to pay off their credit card quickly and immediately using a saved payee as this would reduce interest payable on the transaction. It’s less of a problem than it used to be, now fx fee-free debit cards are more widely available, but may still be required in an emergency, etc.