I’ve been using Monzo (Mondo) since March 2016. I’m a Plus user and Business plus user. I’m user number #5658 and an investor.

Which makes me shocked that for some reason I’m not eligible for a joint account. I’ve gone through support and for the first time was disappointed with the response that “They cannot tell me why I’m not eligible”

Does anyone have any ideas as to why this may be? I’m getting married this year and a joint account is a big requirement for a bank account.

I wouldn’t want to move to another bank, but it may have to happen

I don’t think that Support, or Monzo generally, are doing themselves any favours here

From what I can see, it’s not like you’re illegible, it’s like they’ve chosen to withdraw the product for most people. I think it would be better to say “we’re not offering joint accounts at the moment” rather than to say that you’re ineligible and then refuse to discuss it. That’s just a bank hiding behind bureaucracy and isn’t in the spirit of Monzo at all. In fact, it makes me pretty cross.

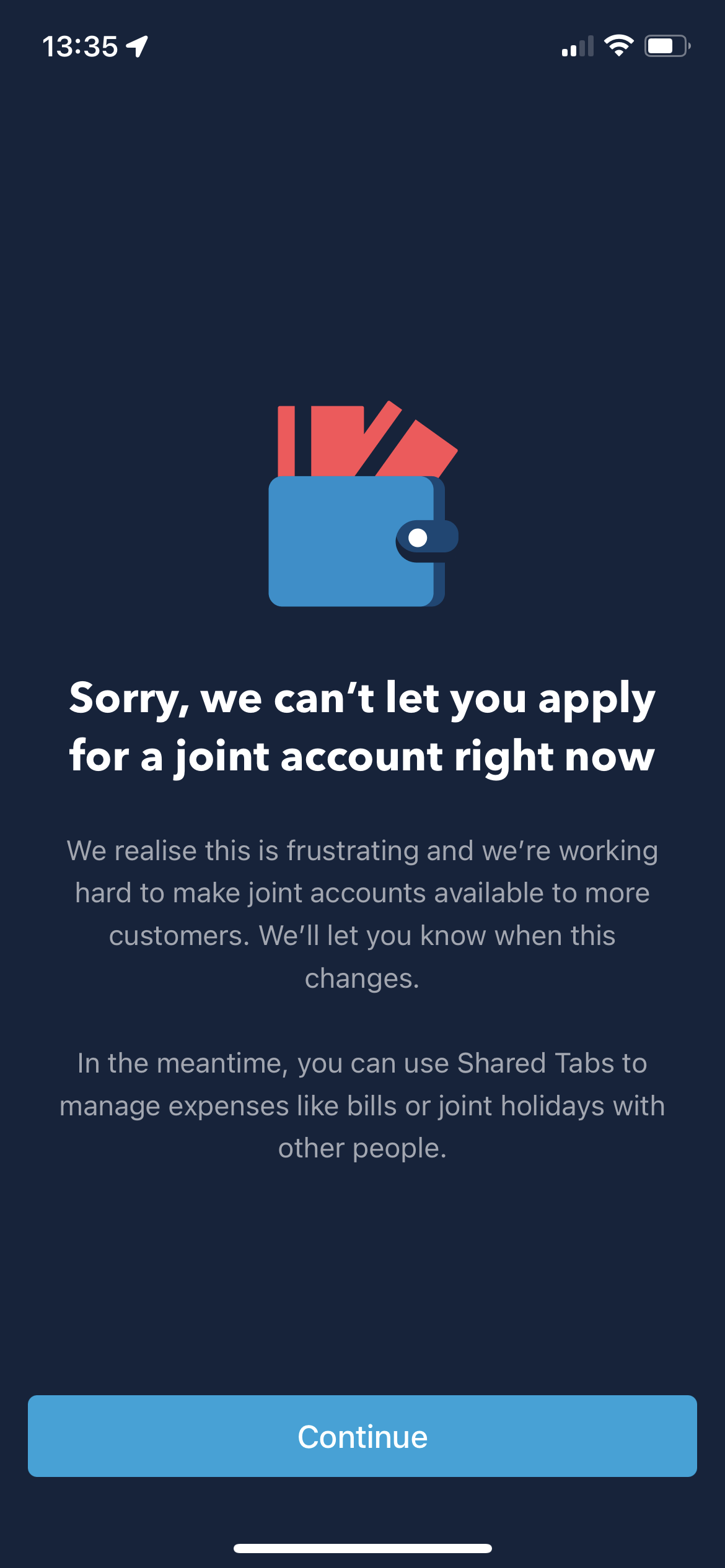

That’s not quite what’s happening here though. It’s not like you can click through apply and then find that you don’t meet the criteria: the option is hidden then when you find it through Help you can’t even apply. That’s what the image in the first post says - they won’t even let him apply.

I think it’s disingenuous and below Monzo. I don’t like it. At all.

I know that because that’s what happens when I look for the option for a joint account. And that’s the screen I see.

I don’t know what “circumstantial” adds here. It is clear that there is a large number of users that Monzo is refusing to consider as customers right now. Now, it’s a reasonable hypothesis that anything so wide ranging would be less about the applicants themselves (particularly as they’re still eligible for Monzo accounts) and either Monzo’s ability to service them, a regulatory reason that’s likely unrelated to customer attributes or a business decision by Monzo. Again, their in-app copy and support responses lets them down and appears to blame the customer when it’s not their fault.

Now this is interesting - thank you for confirming. I did wonder if actually no one was eligible given the lack of data, but it’s useful to disprove that as a hypothesis.

I fear we’re talking past each other a bit, so will duck out after this.

I don’t think the Centurion Card analogy works. Firstly, the Monzo joint account isn’t supposed to be exclusive, the Centurion card is. But more importantly, and the point I’ve made a few times now, is that you can’t even apply for a joint account. It’s not like you apply, you’re assessed with your partner and are accepted/rejected. Monzo is simply not accepting applications from some (many? We don’t know) customers for reasons that are unclear. We can quibble about whether that amounts to withdrawn or not, but it’s all the same for the people affected. And the official explanation (which isn’t really one) doesn’t do Monzo justice, in my view.

They never do. We’re not a particularly representative bunch. But they can offer some fun or some lines of enquiry. It’s up to each of us whether to engage.

The only thing I’d add to your theory is that it might be less that Monzo ‘decided’ and more that it was something they had to do as part of the ongoing regulatory investigation that we know exists but have heard little about otherwise.

Reason I think this is a factor is, Monzo must have had their hand forced in some way because it doesn’t make business sense to turn potential customers away otherwise.

I just tried to sign up. Like the OP I’m an early user and also fairly sure that I have a very low risk profile.

I have no idea what criteria they’re using and they should at the very least fix their wording and make it clear what the reasons are instead of hiding behind this ‘computer says no’ experience redolent of a big 5 bank in the 90s. I also couldn’t leave this JA flow once I entered it and had to force quit the app.

This is a bad customer experience and monzo should fix it even if they can’t fix the underlying problem for regulatory reasons (which I sincerely doubt). Like the terrible experience with transfer allowances (now fixed) complaints like this one help surface bad experiences and help monzo improve their product. They are a good thing and should be encouraged and feed into the decision making process as one input.

The best outcome here is complaints force monzo to focus resources on whatever their problem is that is stopping them offering joint accounts and fix it. Offering products only to some customers is a bit lame, if they’re doing that the criteria should be made clear. It’s worse than just temporarily withdrawing the product for all customers.

Really appreciate all the replies. It seems I’m not the only one.

From reading the other replies it looks like the issue(s) are

Monzo’s wording and experience is bad, whether it is their fault or not

The problem could be with Monzo’s policy or a regulator but we don’t know

The criteria doesn’t seem to be having an effect on everyone, as some people still have the option to open an account

(For clarity - the option doesn’t appear to me, I only get to the screen in the OP through the help section)

I was gonna vote for option 3 (‘N/A - I already have a joint account’) but then had an idea.

We already have a JA - and the options to apply for a JA no longer show in the main feed or the ‘Things you can do with Monzo’ carousel section - which makes total sense.

But what if I searched for ‘Opening a Joint Account’ via help as per above? Well, it found the Opening a Joint Account section, which included the blue ‘Open joint account’ button for me. So I tapped on it out of curiosity and this showed: