I’m brand new to Mondo and have been waiting about about 5 weeks for my countdown to run out before I can order a card. This is now done, but I’m concerned about opening an account as I feel Mondo basically has no documentation or even Getting Started information. Their terms are really pretty vague and there are key details that are not explained in their advertising or on their sign-up pages. Before they even become a bank, I think the ASA are going to have huge issues with some of their operations. I do completely appreciate this is a beta, but you are still handling real money. I’d just like to raise the following and ask if people have any views.

There basically is NO documentation. There’s no FAQs other than those about Mondo itself and not card operation, there is seemingly no customer support other than through the community and there is NO documentation about how the product works, your rights and your responsiblities.

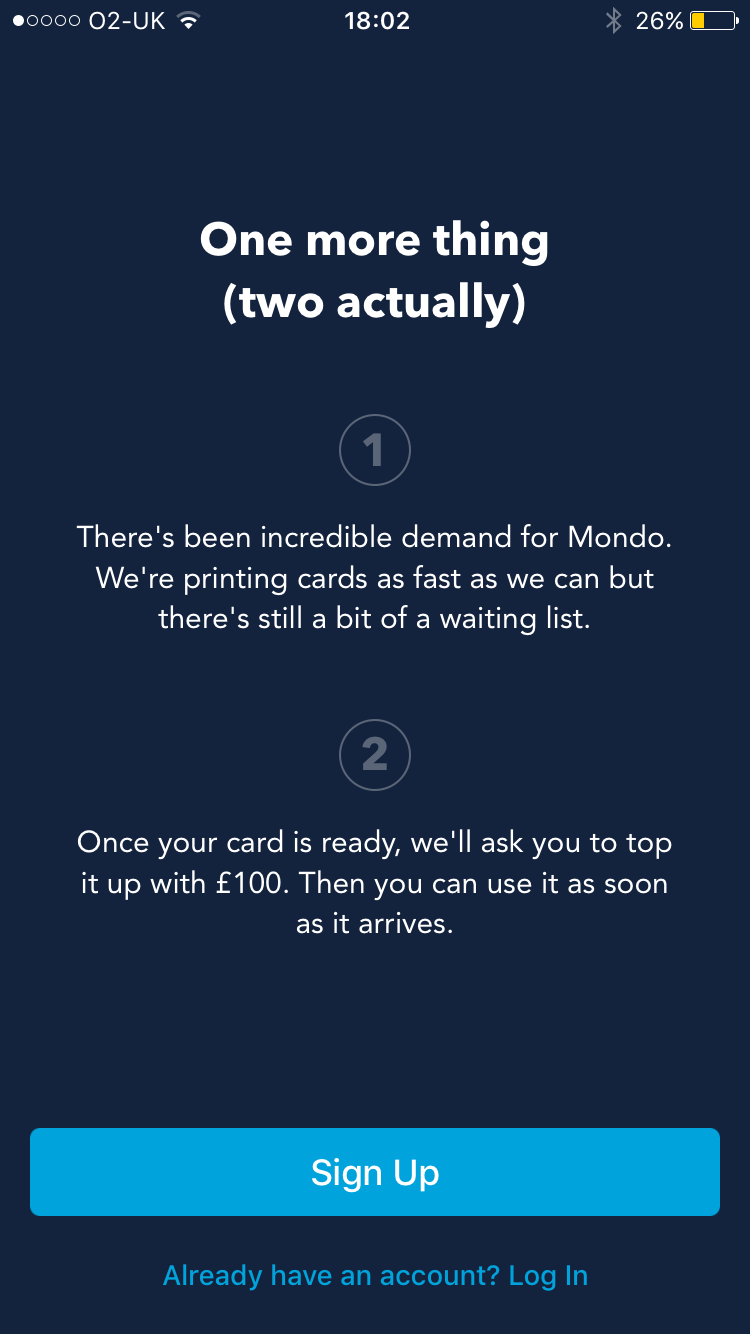

There is ABSOLUTELY NOTHING in advertising or in the signup process about the £100 deposit that has to be made at the end of the queue. There is also nothing about the £50 minimum top up (this was raised as an issue by the looks of it 6 months ago but hasn’t moved forward).

The information about your money protection is MISLEADING. The about page first says “During our Alpha and subsequent Beta testing periods, your money will be held in a separate, protected account by Wirecard, our issuing bank. In the unlikely event Wirecard were to become insolvent, your funds would be protected against any claims made by creditors. All card transactions are processed by the MasterCard network and are protected by MasterCard rules. Additionally, we guarantee that you will never lose money as a result of any mistakes or problems we make while testing.”. It then says “Your money will be held by Wirecard Card Solutions Ltd. (WCDS) who are authorised by the Financial Conduct Authority (FCA) to conduct electronic money service activities under the Electronic Money Regulations 2011 (Ref: 900051). The card itself is an e-money product and although it is a product regulated by the Financial Conduct Authority, it is not covered by the Financial Services Compensation Scheme. In the unlikely event that Wirecard Card Solutions Ltd (WDCS) becomes insolvent, your funds may become valueless and unusable, and as a result you may lose your money. However as a responsible e-money Issuer, WDCS ensures that once it has received your funds they are deposited in a secure account, specifically for the purpose of redeeming transactions made by your card. In the event that WDCS becomes insolvent funds that you have loaded which have arrived with and been deposited by WDCS are protected against the claims made by creditors.” THIS IS MISLEADING and makes your guarantee basically worthless and unenforceable in a court of law.

The only way Mondo can promote themselves a ‘different bank’ is by saying they have no protection and very little clarity.

As I said - I get it, this is a beta. But this isn’t a financial institution. You are essentially an unsecured creditor to Mondo if you use their services and they NEED to make this clear rather than making you wait 5 weeks to be told for the first time you’ll need to deposit £100. I wouldn’t mind if they’d said this at the start but they simply didn’t and as a result this is FALSE ADVERTISING.

I’m sorry to rant, but you clearly want feedback and I really can’t decide whether to proceed taking out a card at this point. Please fact check me - if I’m in any way wrong, please correct me as I hope I am wrong!

Really sorry you feel like this That’s totally our fault. In the interests of transparency, I’ll try and give you an answer to each bullet point — please remember this is why we call it a beta and things won’t be perfect. But hopefully you’ll see an improvement over time

We’re going to be updating and improving our FAQs in the very near future. I’d love to know what you’re looking to get in terms of documentation specifically so we can add it

As soon as you have a card, we have 24/7 chat support and our current median response time is less than 10 minutes (off the top of my head). Additionally, you can email help@getmondo.co.uk at any time if you can’t access the chat support. We should make that clearer though

When you get a card, you’ll see that info on the back as well as a direct phone number to our customer support team. However I recognise that this is mainly once you have a card and so to have the feeling you have before you get a card is definitely not something we want! We’ll work on it.

Yep, agreed! That’s actually already been changed as of the last app update and we tell you about the queue and the initial top up before you signup It wasn’t clear enough before and that was our fault. The minimum top up is £10 once you have a card.

I’m not a lawyer. But the line saying “Additionally, we guarantee that you will never lose money as a result of any mistakes or problems we make while testing” is one we’re committed to and have lived up to with customers in the last few months when necessary. It’s over and above the legalese we get from Wirecard. Maybe we should make that clearer?

Thank you for the feedback. Seriously. I know that’s what most companies/institutions/banks say but I really believe that we really mean it. I’ve sent this to the rest of our product team to take a look at too but I hope we’ve actually fixed/improved on all of your issues in the last few months and especially with the latest update Please keep the feedback coming!

Hi Alex, thanks for taking the time to share your feedback. I know it’s not always an easy thing to do The one thing I would like to clarify is that you are not an “unsecured creditor to Mondo”. We never get to touch the money and nobody is borrowing it from you.

Wirecard is simply holding the money for you. They don’t get to invest it or use it in any way. You are the owner of a prepaid debit MasterCard issued by Wirecard Card Solutions Ltd. Wirecard is a licensed e-money issuer. We are but one of many prepaid card programs that Wirecard issues cards for and we offer the same guarantees as any other prepaid card.

Your money sits in a ring-fenced account that Wirecard controls. In case they go into administration, Wirecard’s creditors do not have access to your money and you will get it back. We cannot, however, prevent Wirecard, or even the bank they store your money in, from losing your money through negligence or to criminals. That is why we have to warn our customers. We were told that it is safe to tell our customers that money stored on a prepaid card is “safer than cash”. It is just not insured by a third party in the same way balances on a current account are (although we do offer that informal promise that Tristan mentioned to cover any losses from our own pocket)

Hi Tristan and Jonas, thanks for your speedy replies!

Some really valuable responses there. I’ll go ahead and respond to each point below.

Yes - definitely. This is good to know - I think this ideally needs to be prominent on a page entitled ‘Support’ so there’s clear accessability to key information there.

Again, definitely. I think that if you’re required to hand over a £100 deposit to secure the card, there should be someone you can call to get support afterwards just in case anything goes wrong. I wouldn’t say it necessarily has to be prominent on the site as I understand Mondo is trying to move away from a telephone banking approach, but I think access to telephone numbers will be key to some (including me). A phone number gives me confidence when buying online - even though I might not use it it’s good to know it is there if you get what I mean.

Good, definitely needed clarifying! You might find find your signup queue gets a bit easier to process now!! EDIT: The Mondo app suggests a £50 minimum top up in the T&Cs - does this need clarifying?

For that matter, there should be a link to the Terms that’s visible from my website in my view - there should be a Terms link on the homepage that points to www.getmondo.co.uk/terms.

I think it should perhaps be clearer and again ties in with the support issue. I think you need to have a support document that explains what happens if things go wrong and this should be in plainer English in your T&Cs. You need to make it clear that while you’ll do everything to can to mitigate risk and ensure money is protected, you are offering a product that’s managed by another cardholder. If Mondo went out of business (not that I’m saying it would at all), the only person I can go to with a hope of getting my money back is wirecard - there needs to be more information about how I can speak to them if I needed to as a last resort, I think.

This is what you need on the aforementioned support page. You must also be careful, as you have said yourself, that it is an informal promise and would you agree with me that “informal promise” doesn’t define the same way as “guarantee”?

Thanks for your clarifications guys, happy to provide any more feedback if you’d like it. I would really like to join Mondo and will definitely consider it, just having a bit of Martin Lewis moment if you get my drift!

I don’t know how feasible it would be to email all the waiting queue with something like

some time scales - if you are number X in the queue that will normally be dispatched to you in X weeks …etc + you will need to top up your card with £100 before we dispatch it to you because …etc which will be immediately available for your use to see how great the card is etc etc etc if you no longer want to be a Mondonaut - unsubscribe from Mondo Queue etc

an informed queue is a happy queue

some of the new user “complaints” on the community forum over the past couple of months have been the lack of info or indeed knowledge regarding the initial top up - this would help everybody , the people in the queue who don’t have or don’t want to top up the £100 could have their email removed from the list and the queue would get shorter for those willing to commit the 100 quid therefore getting their card in a shorter waiting period.

T and Cs have also been discussed over a period of time , and whilst I appreciate Mondo are busy with Licences , bugs, promoting etc etc etc - these should be correct and up to date - sorry @anon50039658 it does say somewhere that customers will be given 2 months notice if these change - they really do need sorting out as quickly as they can be.

I invested in the crowd cube funding round , and am very happy that I did.

Having said all that Alex, you will be pleasantly surprised with how good the app is should you decide to take the “risk” because it is a great card which Ive experienced over the past 7 months with very very few problems , which have been sorted out within reasonable time periods

And I can confirm that Mondo have made a huge improvement to the clarity and transparency of the initial user onboarding process in the last couple of weeks. Just log out to see it

Hi James , I have seen them now , which is great that new users are being informed when they download the app in the small print that they have to top up 100 quid to “activate” the card - from some of the negative comments in the reviews of the app on iTunes it seems that some of us “cough” don’t read all the details on the app though - duly chastised … lol

I must admit I was a bit dubious about putting my money into Mondo. However, since speaking to support a few times via the app and using this forum, I’m happy to fill up my card as much as possible.

The whole way it works is so refreshing to see. After reading through the Ts&Cs yesterday I was worried about that lack of security for my money but it would appear it was just simply poorly worded.

A friend of mine downloaded the app the other day, and the whole signup process outlines that you have to load the card with an initial £100 which is great (good job, team!) and it also outlines a few other key things so the team are listening to feedback (again, refreshing to see).

I cannot wait for Mondo to be a fully fledged bank, because I will be closing all other accounts straight away!

I absolutely agree with @anon95680666. Please think about sending emails to inform people in queue of progress etc. I am still in the queue and signed up before the latest changes were made and if I wasn’t interested in learning more by reading the forums then I’d be none the wiser with the £100 activation fee and all the rest of it and have maybe forgotten all about Mondo by now. A weekly email update would be hugely appreciated. It can maybe have a note of what number I’m at now, along with some tips or features or “things to look forward to once I receive my card” type thing.

Clearly a lot of people think 100 GBP are gone before they even start using Mondo. Perhaps a more clear explaination on that initial top up would be great for new users during sign up process. A clear illustration (with the Mondo character) would be attractive and interesting!

as @anon64350903 says _ "activation FEE " there is clearly a lot of confusion about this 100 quid remaining as yours to use straight away once your card arrives - a few people in the review pages on iTunes think they have to pay £100 for the card and they presumably don’t take in the information on the One more thing (two actually) screen - a lot of people read the negative comments on iTunes reviews first before all the 5 star ones

Exactly! Lack of a better term? I think I’ve been in the queue about 3 or 4 weeks now and I honestly don’t remember what any of the screens said. I only found out about the £100 by seeing it mentioned in the forum and I’m only confident in seeing that money again because Mondo has been personally recommended by people that actually have the card. Which brings me to the bizarre point of the 4,000 places for referral… how can I possibly promote something that I’ve never used myself?! I mean… I am doing it… I’m excited about it… But I think this comes from being referred to Mondo from someone who knows someone with a card and having the interest to follow the forum. How would someone I refer have that same confidence? I definitely think more information needs to be available and not just tell people to go search the community forum for more info. Or maybe this is an interim way to slow the beta process?

I didn’t know about the £100 top up when I joined the queue but when I found out I wasn’t entirely surprised , after all it’s a prepaid card What would you do with a prepaid card if you don’t top it up? A £100 is not an unreasonable amount, it gives you enough to test out whether the Mondo card actually does what it says. People seem to spend so much time analysing every word of the T&C’s but fail to understand the basic principle of top up. The word too was ‘top up’ not ‘fee’ so I was quite confident that it was not a detriment to me.

I’m as blind as most people rushing headlong into things without reading all the user guides but at just four days in I’m over the moon with what Mondo has done for me so far. I’m happy with the level of instant control of my finance level that Mondo gives me and I’m more than happy to keep on trialing it. When it becomes a bank though I would have to seriously consider transferring to Mondo if they provided the full basic services I needed. If of course they’d have me As a pensioner after taking early retirement I don’t get a lot of money so if they instigated minimum monthly pay-ins I would probably fall below that. In that case I’d have to hope that they kept the prepay option

That’s totally our fault. In the interests of transparency, I’ll try and give you an answer to each bullet point — please remember this is why we call it a beta and things won’t be perfect. But hopefully you’ll see an improvement over time

That’s totally our fault. In the interests of transparency, I’ll try and give you an answer to each bullet point — please remember this is why we call it a beta and things won’t be perfect. But hopefully you’ll see an improvement over time

What would you do with a prepaid card if you don’t top it up? A £100 is not an unreasonable amount, it gives you enough to test out whether the Mondo card actually does what it says. People seem to spend so much time analysing every word of the T&C’s but fail to understand the basic principle of top up. The word too was ‘top up’ not ‘fee’ so I was quite confident that it was not a detriment to me.

What would you do with a prepaid card if you don’t top it up? A £100 is not an unreasonable amount, it gives you enough to test out whether the Mondo card actually does what it says. People seem to spend so much time analysing every word of the T&C’s but fail to understand the basic principle of top up. The word too was ‘top up’ not ‘fee’ so I was quite confident that it was not a detriment to me. As a pensioner after taking early retirement I don’t get a lot of money so if they instigated minimum monthly pay-ins I would probably fall below that. In that case I’d have to hope that they kept the prepay option

As a pensioner after taking early retirement I don’t get a lot of money so if they instigated minimum monthly pay-ins I would probably fall below that. In that case I’d have to hope that they kept the prepay option