It said something like that on the email, but I was adding to the hypothesis that monzo had got stricter recently because I’d never seen that email before I think.

All banks are required to keep records of their customers for a certain period, I think it’s seven years. Even if you close an account, they still have to keep the records until this period expires. It’s not like closing J Random Onlineplace account where they will wipe all your records straight away.

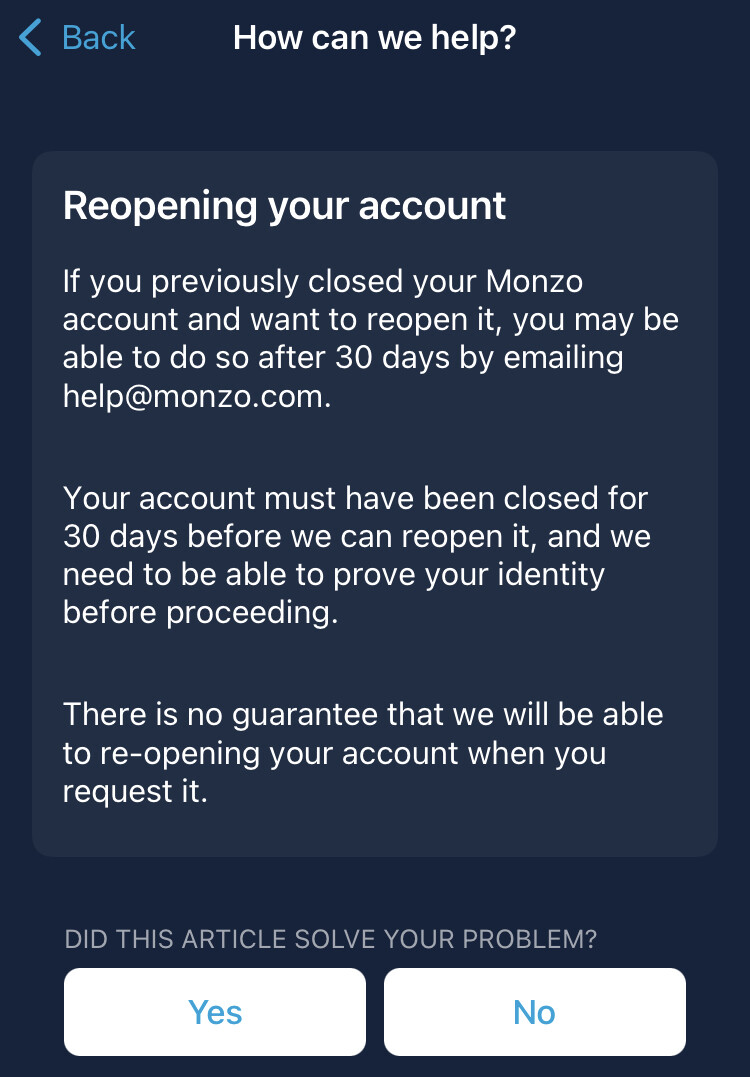

It’s unlikely Monzo will ever give a straight answer (because explaining how their systems work to this level will give bad actors the knowledge they need to game the systems), but I think this is probably the main reason you can’t re-open your account.

Whether it’s closing an account in and of itself that sinks one’s chances, or whether closing an account results in a big negative being added to the risk scoring that requires much higher scoring everywhere else to cross the bar (which would be why same scoring as new was OK, but same scoring with account closure is not), I don’t know. Again, the above applies re: unlikely Monzo can reveal this.

On another level, it must be mentioned that banks are not obliged to take people as customers. If customers are able to say “No, you’re not the bank for me”, it’s really fair enough that banks are allowed to say “No, you’re not the customer for us.”

I was full Monzo for a while around 3 years ago but CASSed away. I had no issues opening a new account this time last year - just asked if my mobile number could be deleted.

Banks are required to find out where the money our customers hold comes from, and how they intend to use it, as part of what’s called ‘customer due diligence’.

Asking about sources of income (like salary, pension or investments) and what that income is (the actual amount of money coming into your account on a regular basis) helps them better understand you and how you’ll use your account. It also helps keep your account safe because it gives us a baseline which we can spot ‘unusual’ activity from.

I feel left out. Can’t remember the last time I got asked by any bank, but they do ask this stuff when you sign up so it’s probably for those who have had their accounts longer.

I went through so much hassle - couldn’t offer me an account so I wrote to the reviews team and they overturned the decision. Was stuck on the verifying screen for a good 3-4 days just for them to write back again and revoke said decision, not offering me an account anymore. No clue why but doesn’t look like you can reopen accounts with Monzo after you leave!

It was open for about 10 days, but it was never used - no deposits at all, but I had ordered a physical card in expectation that it would become my main account. I just decided I preferred Starling so I closed the Monzo account in-app.

Easier said than done for me. Many lifetimes ago I had some problems with gambling which, thankfully, I managed to get past but I learnt to identify certain triggers and move away from them and in the case of Revolut, it’s access to Crypto. I’ve already gone down that rabbit hole one too many times so it’s something I need to get away from.