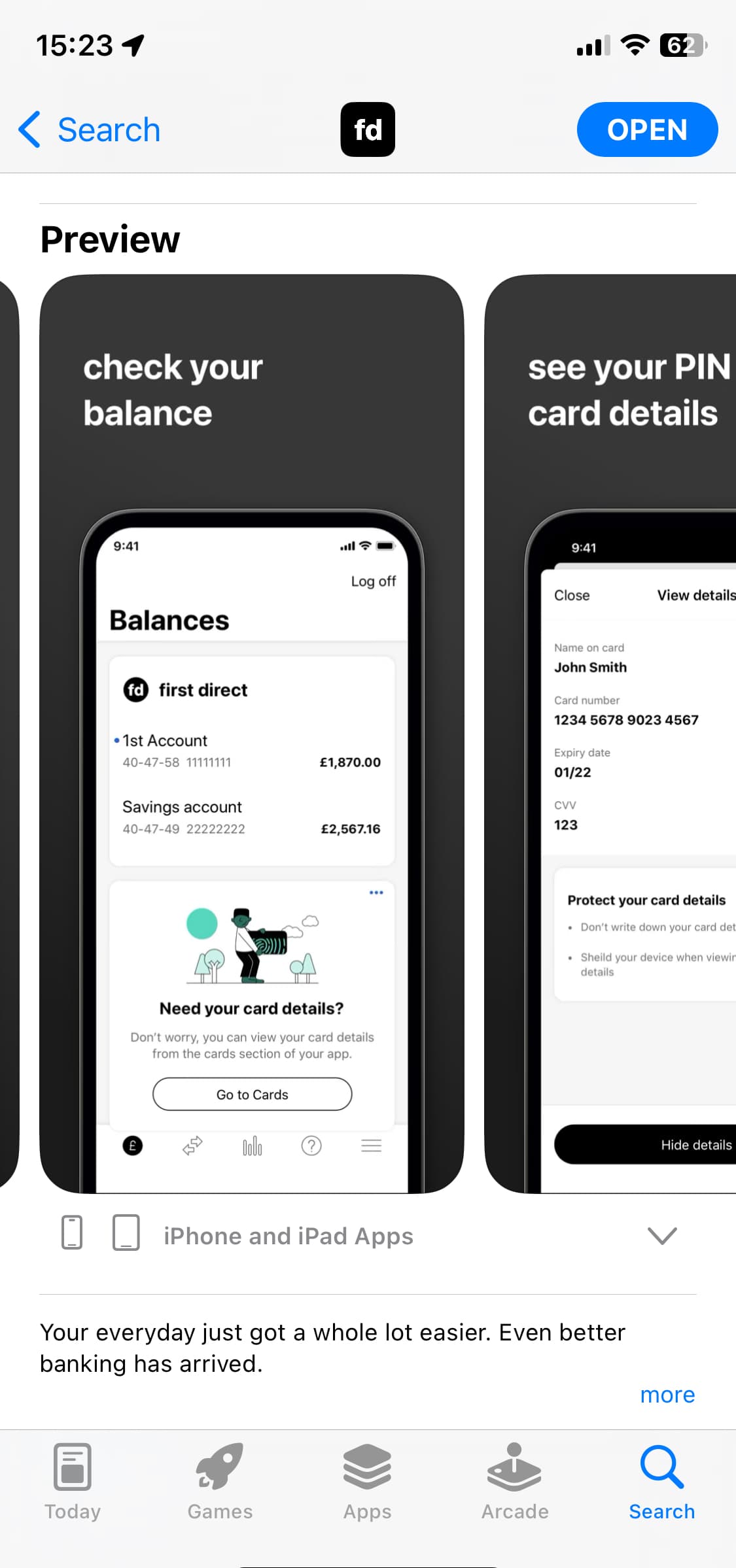

FD appear to be attempting to look all modern with their latest screenshots. I think they look quite nice.

Although, I’m not sure how transactions that don’t appear until they’ve posted can be classed as “real time” ![]()

FD appear to be attempting to look all modern with their latest screenshots. I think they look quite nice.

Although, I’m not sure how transactions that don’t appear until they’ve posted can be classed as “real time” ![]()

Feels unnecessary, could have just PDF’d and made them available in the app. Guess I’m not their target demographic but the switch offer was too good to pass on.

For you (and me) yes but for a number of FD customers that’s how they like to roll otherwise I imagine they would’ve done away with them years ago.

I’m sure all the youths of today use first direct

Also considering insights are not real time nor can you budget I’m not sure what their plan with this one is.

![]()

/ˈfeɪspɑːm/

Anyone bothered opening the 7% regular savings account? I’m just wary that in case a better rate account is provided by another bank, I close it before it reaches maturity, I’ll get a measly 0.65% instead.

Nope cos the Barclays rainy day saver covers this base. If and when I have more than £5k in savings I might.

I’m greedy.

I have both ![]()

My other concern is getting taxed on interest in the new year with all these high interest accounts.

I’ll be getting taxed again.

Just need to live with it tbh.

It’s an easy process.

I’ve read HMRC are informed by banks as to how much interest they’ve paid out and HMRC adjust the tax code accordingly? If you’re on PAYE is that right.

Yes. That’s exactly how it’s done ![]()

I think it is ridiculous for the government to tax interest, especially with such high inflation. Say you are a higher earner and you earn £700 in interest, you are taxed 40% on £200. But that interest is actually partially offsetting inflation, to partially maintain the value of your savings, so why should you pay tax on that?

The thresholds ought to be increased (though not removed). [Appreciate that there are cash ISAs but that is besides the point].

Freeze of thresholds is intentional government policy to raise tax revenue.

They know they are taxing inflation.

There used to be inflation uplift of cost basis to reduce tax paid on disposal of assets (i.e. capital gains tax) and that has been scrapped a long time ago.

Politically it is intentional stealth taxation.

After a few weeks of no adverts FD have suddenly started to push them through again

Some are useful, others perhaps not. I’ve had the account for two months now so I’m pretty sure the card has arrived!

What’s irritating is when you click Don’t show again, and it continues to do so ![]()

One of the reasons I favour Starling over first direct/Barclays/NatWest is that I don’t have to deal with any inane boxes of fraud advice/adverts/product launches.

I agree. The strange thing is for me at least I didn’t get any for months. Just login and check balance. Simplz.

But now I get them every time, which is…irratating

They come and go on android. Granted I don’t use the app, I do check now and again to see if anything has changed and at times I will get repeated pop up things under my accounts, even ones I’ve said don’t show me again.

I just pulled to refresh and selected “do not show again” on about 15 of them, will see how long it remembers that for ![]()