My name is Kieran and I lead Open Banking at Monzo. While my main role is Backend Engineer, I’ve also been doing quite a lot of product and project management, public policy, and outreach work as part of Open Banking. While it’s the hardest project I think I’ve ever worked on, it’s also been very rewarding and a great opportunity for personal development. I have learned a tonne of stuff!

I wanted to kick off this thread to share some info on the hard work we’ve been doing over the past few months, and how our customers will experience it. In the future, I would like to do some other content aimed at other fintech companies hoping to use our APIs, a dive into the technology that powers Open Banking at Monzo, and how we managed to implement quickly and inexpensively by using our platform.

For those of you who have never heard of Open Banking, it allows regulated companies to access your

account information and initiate payments from your account (with your permission). The core principle of Open Banking is really that your financial data should be yours, and if you choose to, you should be able to allow a third party to access it.

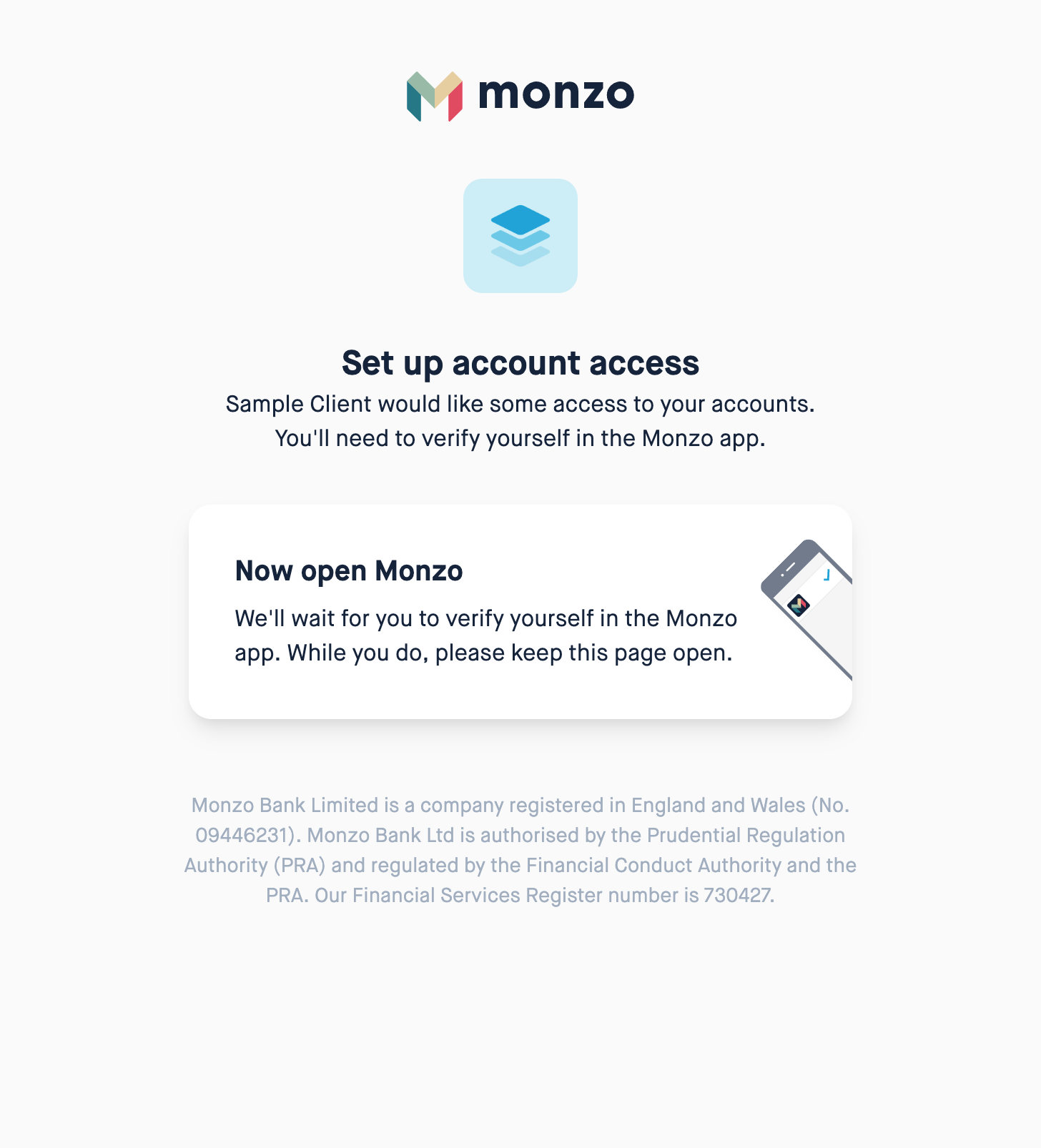

Here’s the sort of thing you might see when granting a third party access to some of your account information on Monzo.

And, likewise, you might see something like this to set up a payment on your account. This is an example of a scheduled payment, but you can also set up immediate payments and recurring payments!

If you’re visiting from a desktop computer, you’ll see something like this. This will send you a push notification and pop you straight into the screens shown above.

There are a couple of “core principles” I think our team think about with Open Banking…

We’ve put a lot of effort into making the connection process as smooth as possible. We’ve designed whole new desktop and app-based flows. We’ll use Face ID and Touch ID if you have it set up. We’re taking advantage of the same awesome cryptography technology put into our app by the Strong Customer Authentication team.

We’re not using the phrase “Open Banking” anywhere in the app. We are serious about not putting jargon in our product. Our customers shouldn’t have to worry about the regulatory framework that enables the connection - or the technical implementation of it. It should just work, and since it’s from Monzo, you know you can trust it.

We’re serious about uptime. Unlike many other banks, Monzo engineers have written our banking platform in-house from scratch. This means we have an incredible amount of control over our Open Banking implementation. We won’t need to take it offline all the time (for hours at a time) for “routine maintenance”.

We’ve implemented the Open Banking Standard, so our implementation has the same external interface as every other bank. This makes it much easier for new companies to connect to Monzo without having to write bespoke additional code specific to us, and hopefully it means Monzo customers can connect their account to all of the same services available to them as customers from legacy banks.

Please Ask me Anything (AMA) about Open Banking, what it’s like to work on, or how we think about Open Banking at Monzo!

overestimate the potential of new technologies in the short term

underestimate the potential of new technologies in the long term

People have had really high expectations of Open Banking, and sometimes it can feel like it isn’t working, or it hasn’t delivered much. I can empathise with this. I think this is all going to change though.

The most common use cases for Open Banking will be almost certainly be “account aggregation” – bringing all of your accounts together in one place. I think every high-street bank will want to do this, and Monzo will too, as part of our vision for creating a financial control centre. Since so many Monzo customers have at least one other bank account right now, Open Banking will be great for us to ‘consume’ as well as contribute to by being a bank.

I try not to have favourites but I really like the idea of CreditLadder which uses Open Banking to report your rent payments to Credit Reference Agencies and improve your credit score.

All banks and regulated companies are part of the “Open Banking Directory” and we use this to keep each other up to date with news. We have told everybody about our Open Banking plans and I’ll be sending another update on Friday to keep everybody in the loop. We have already onboarded lots of companies, and they have been giving us feedback to improve

In terms of making it more intuitive to bring data into Monzo, I will assume you are talking about banking data from other banks. I have some opinions on this, as I was also tech lead on our credit cards in Monzo project, which is currently on hold while we wait for all banks to make their credit card products available on Open Banking. We were using screen scraping before, which was really quite unreliable and generated a lot of support load for us.

We will migrate away from screen scraping and towards Open Banking flows, which will be more reliable. While we do have some control over the experience in our own app, we are limited by other banks’ login interfaces. These have improved significantly over the past 6-12 months as some of them were truly awful before and completely impossible to use. In many cases we will be able to use app-to-app authentication, so you’ll jump out of the Monzo app and into the other bank’s app, and then straight back

Not obviously to feign more knowledge than Kieran, but what I would expect as a customer is to see it in the same area of the application as my approvals of the Android app and IFTTT

This is a broad question but in order for “open banking” to be truly successful, I really believe that customers shouldn’t even know they are using it.

Think about a washing machine. It’s a robot with fairly complex embedded computers, but you don’t see it as a robot, you just put dirty clothes in and take clean clothes out. When things work properly you don’t think about how they work. In fact, if you are thinking about how your washing machine works, you are probably investigating a fault with it!

I gave the example of CreditLadder above. Flux (our transaction receipts provider) is also an Open Banking provider. These are examples of where customers are already benefitting from Open Banking. I think its best days are ahead of it.

To be honest I don’t think Open Banking will be instrumental in driving revenue in its current form, but I think the industry is moving towards “premium open banking APIs” which would allow Monzo to charge companies a fee for access to special information. As a random example, since we have verified the identity of every single Monzo customer, we could charge other businesses to provide confirmation of your identity without you having to give away your passport or driving license information to them. That could be interesting for us, and great for customers, as it would make the process way quicker!

Yes - this will live in our Manage Apps screen alongside IFTTT and other things. You can revoke access at any time, and you’ll also need to re-confirm access every 90 days. But we will make this easy as well.

The main thing will be to expand our existing credit cards offering to current accounts too!

Unfortunately the scope of Open Banking is currently fairly limited and many banks are struggling to cope with even this limited scope. Savings, pensions, mortgages etc are not in scope. But I hope that one day, more products will be available on the API so we can pull those in too.

How much of the work you’re currently doing will affect individuals looking to interact with Monzo? Is there any progress on allowing more than just a whitelisted set of users to sign in to an app I create?

Hello all!

Hello all!