I’ve been doing a ton of research on banks to replace Simple. My husband and I have used the Expenses “buckets” since they were introduced. Our financial situation before them was a bit rocky, and very “paycheck to paycheck.” In the last few years of using them, we’ve really been able to truly get ahold of our finances, never been late on a bill, and haven’t come up short on funds. We’ve built a savings account (technically 2, with Goals), and we’re in a better financial situation than ever before. Plus, I stopped having to use my Excel spreadsheet for budgeting… We tried budgeting sites and apps like Mint, but they still can’t get our transactions tagged correctly, and I’d spend hours fixing it.

Our hearts, and stomachs, sank when we got the alert that Simple is no longer come May… So, I’ve spent hours, days and weeks combing through bank after bank, feature after feature. I’ve done my own searching, and used the Reddit spreadsheet (now a website). Here are the 3 I’ve chosen to compare:

Zeta- Similar to Simple starting out, they’re “backed” by a bank, but not actually a bank themselves. They feature “couples” account features, including funding for bill pay. I’m not entirely sure how it works, but the website features an image of a reminder that rent is due soon, and has the option to fund it.

In addition, you can create your own bucket like savings accounts for yourself or shared between you and your joint account holder.

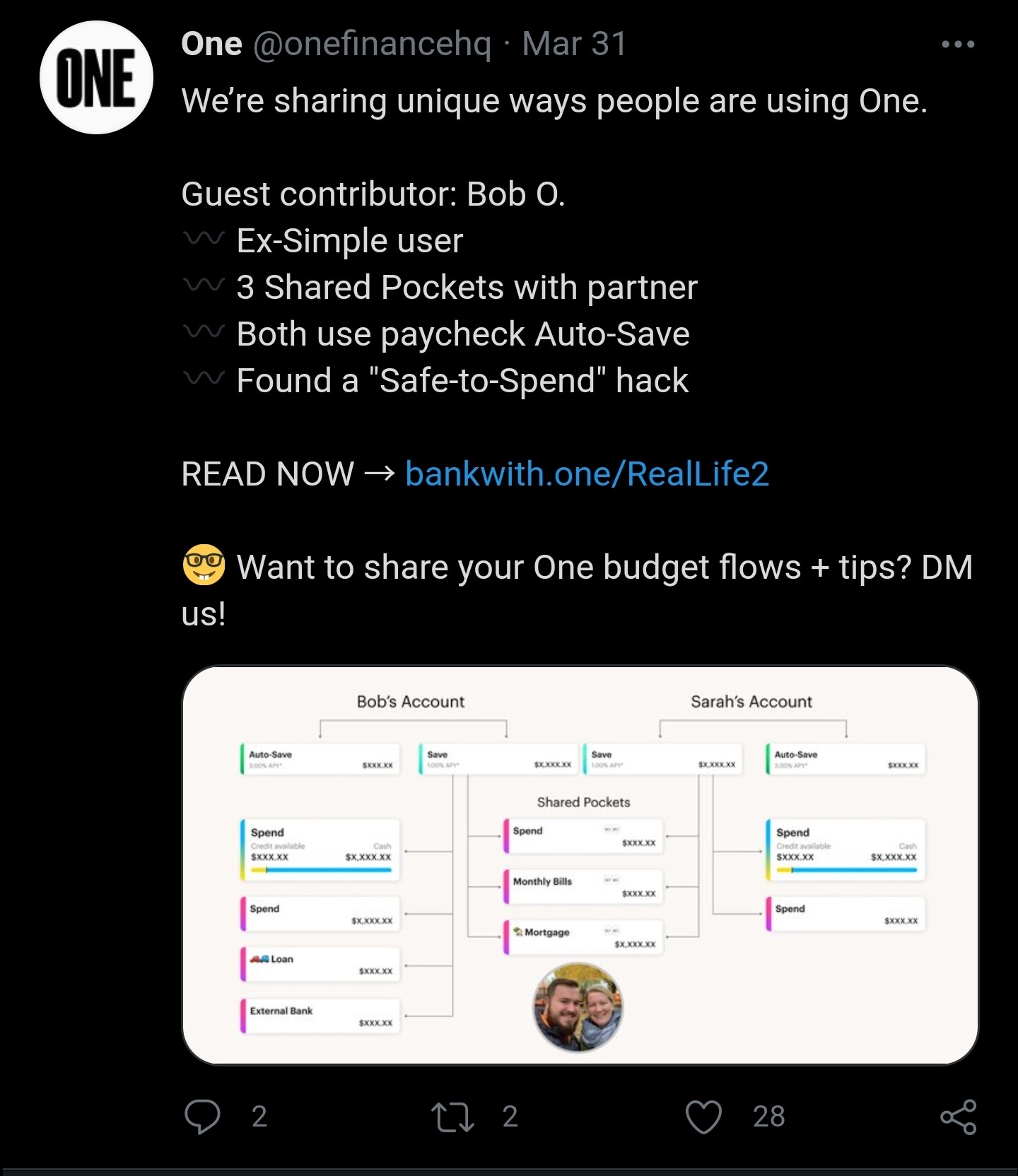

One Finance- This one seems complicated and time consuming to setup, but does seem like it could be a good replacement down the line. One is boasting a direct comparison to Simple. Their twitter account is littered with these, and even suggests their users share their own budgeting flows using One’s “Pockets” feature to compare to Simple.

However, I’ve seen notes that there is no way to setup a “safety net” pocket to fund your spending pocket if you drop below a certain amount (similar to an unprotected savings account). I’ve also heard that you have to actually set your card to a specific pocket before using it, which would make paying your bills via debit card extremely time consuming and complicated (especially with services that solely rely on debit card payments, like Netflix or Amazon services).

That said, it seems as though this might change later down the line with them being so heavy on their comparisons with Simple’s features. In the long term, this could be the bank to replace them, but for now looks very convoluted.

What sets this apart at the current moment is the auto savings APY (3% up to $1k, and 1% on the savings account up to $5k), and ability to share “Pockets” with other account holders. It removes the need for joint account holders, and expands the ability to share money. Their “Boost” feature seems like it could be a very powerful tool as well, which finds places where you can save automatically as well as tracking your spending habits.

Then there’s Monzo. I’ve seen other banks that tout bucket saving, including Ally (which is a strong competitor even without the Expenses feature), but without automated spending from these buckets it’s just not as much of a draw. I’m very curious how Monzo handles this feature, or how the IFTTT automation can be set to handle this.