Did not realise this was still the case, wow! ![]()

I was shocked at how long they didn’t support Apple Pay, and would never have got my rewards card if that was still the case.

That they still don’t support google pay… just wow…

Did not realise this was still the case, wow! ![]()

I was shocked at how long they didn’t support Apple Pay, and would never have got my rewards card if that was still the case.

That they still don’t support google pay… just wow…

Ah yes, Pingit, I had that for a while and I agree, it seemed to be what they wanted but then someone veto’d it. Much like Bo with RBS/Natwest

Yes, the fact that Android allowed open access to the NFC chip was the killer thing that kept them promoting “Contactless Mobile” instead. For a while, when they were holdouts with Apple Pay, I thought they were waiting for pressure from banks and/or regulators to force Apple to also open up NFC. Once they didn’t, and various investigations into it got dismissed, Barclays finally caved in as they were the only major bank not supporting Apple Pay and were probably losing customers as a result. The other big example of banks attempting to pressure Apple into opening up NFC was in Australia, where initially all the big banks refused to join. Subsequently, they did all join and their efforts to fight Apple in court failed.

Yes, I had it too and it was an interesting experimental app. I also registered by phone number to Pingit with Paym but now have Paym registered to a traditional bank instead.

I think both Bó and Pingit were serious incubation strategies at one stage, before ultimately it was decided that rebuilding a banking platform from scratch was just going to be too costly to do. Barclays also had Launchpad, of course, which used to be more active when it was a standalone app. It’s still there in the main app now, but doesn’t seem to be used for much these days.

Are we seeing innovation slowing down as traditional banks decide they’ve reached the point of “good enough”, and fintechs are putting more of their new and innovative features behind paywalls in an effort to monetise? It does feel like we are a bit.

I certainly think the “innovation gap” is shortening - which is going to make it increasingly harder for the fintechs to remain relevant in.

It’s certainly going to create cost pressure for them.

Until now, all of the cost pressure has really been on traditional banks who have been forced to maintain costly branch networks and ageing infrastructure (because it’s too difficult to move off it) whilst also needing to invest significantly in IT to try to catch up with fintechs. At the same time, fintechs have been in early-stage growth with investors eager to fund them due to future potential.

Now we are entering into a different period, where it is seen as more acceptable for traditional banks to be reducing their branch networks (post-Covid) due to declining use, which will save them significant sums. We are also seeing how the sprint to catch up, technology-wise, has paid off - with most key features like notifications supported by the majority of banks in some sense, and probably in a way that’s “good enough” for most customers even if it doesn’t truly match fintechs yet.

Meanwhile, fintechs are starting to feel pressure from investors who want to see profitability and returns, so they are no longer innovating at breakneck speed or seeing such rapid user growth (because the initial early-adopters phase of rapid growth is over). The honeymoon period for investors is therefore ending and they want to see results. This has led to a relentless pressure to monetise which is the driving force behind most new features nowadays (Plus, Premium, Monzo Flex) but these new features have less of a wide appeal to customers, with many of them arguably quite niche, and they also aren’t free - so act as less of a draw to customers who need persuading to move away from traditional banks.

I would say that Monzo, Starling and Revolut (at least) have established themselves as a long-term presence in the UK market, and have a secure future, but we may as customers not see the same levels of rapid innovation again unless something else comes along to cause a market upset. It is possible that things are settling down to a “new status quo”, if you like.

They still don’t support Apple Pay on all their cards. The new Barclaycard Avios cards have been released without Apple Pay support, for example.

Some others without Apple Pay support here

New: criminals abusing Apple Pay and going on spending sprees. Possible because of bots that call victim and get their 2FA code to add their card to Apple Pay, other contactless systems. Fraudster says Apple Pay is “easiest” way to make money w/ these bots

I think this belongs over here:

This is the most interesting statement for me;

Financial Ombudsman complaints data show one in three accounts frozen so far this year turned out to be ordinary customers going about their financial lives perfectly legally.

Frozen is fine, banks just like to check, if they’d said banned and closed, then I’d think it’s unfair.

For the banks. But it’s important not to lose sight of

The frustration, panic and financial hardship it can cause legitimate account holders is immense…

And

The disruption caused by account freezing is significant. Direct debits and standing orders are frozen and customers cannot withdraw any money. Bills bounce, credit is impaired and in extreme cases individuals and whole families are left financially destitute for up to 42 days.

I’m not saying that the banks are doing anything wrong, some level of false negatives is almost inevitable. Also, while customers who are genuinely innocent are probably more likely to go as far as complaining to the Ombudsman, I’m not sure that a two out of three hit rate should be acceptable, either. There is either something wrong with the system, or it’s implementation.

There’s good advice at the end of the article, though.

… the best protection is to have more than one bank account.

I agree with you.

There will also be a significant number of customers who just don’t bother to complain at all, who are still innocent, and therefore won’t be counted in the figure (even though, if you are innocent, you are more likely to complain as you suggest there will be some who don’t). This means the true figure of affected innocent customers is likely to be even higher.

The “guilty until proven innocent” approach also doesn’t work, as you say. Not only does it reverse the usual presumption of innocence, but it also can inflict real hardship on affected customers through no fault of their own and seemingly randomly - there is deliberately no warning of it coming.

To be honest, I’m aware of that risk myself so I always keep at least two or three accounts with a bit of a balance in so I have other alternative emergency accounts. But how many people do that? Not many, when a huge number of people still only have one current account full stop.

In classic Chip fashion, nothing they “build” is built in house, proprietary or well designed. They’re just a plug and play skin on other propositions.

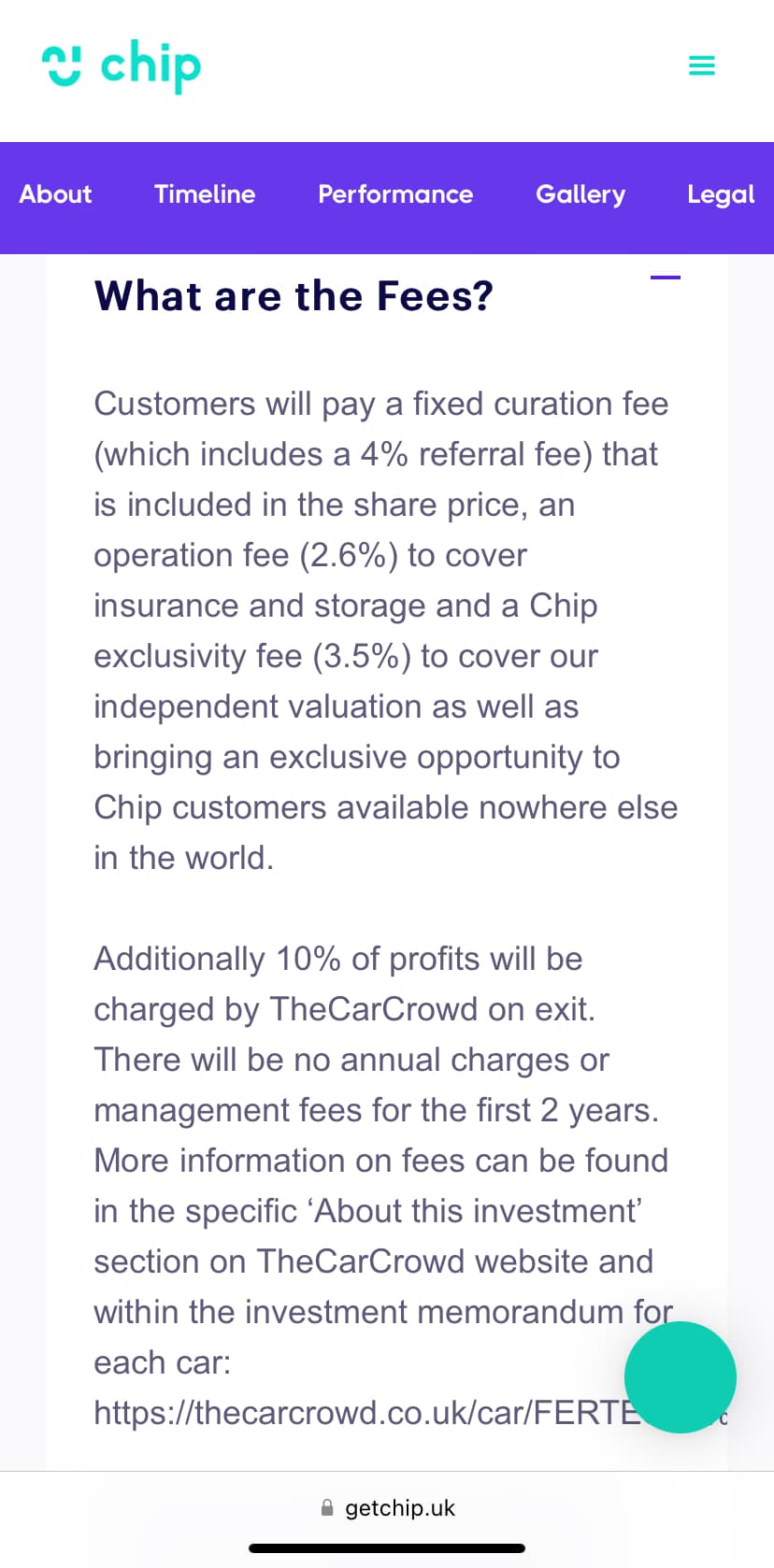

The fees are insane, the mechanics are illiquid/convoluted and tbh I don’t even understand why they would pursue this as it doesn’t strike me as scalable to a critical mass of users to even move the needle in revenue generation they need to be viable:

https://www.getchip.uk/invest-in-cars/ferarri-testarossa

This reminds me of when they wasted crowd investor money and time building the ChipX Peer 2 Peer platform that never made it out of alpha testing. Their crowdfunders will be burnt the same way MoneyDashboard crowdfunders were.

Well at least Chip seem to be more transparent, even if it will end (probably) as you state above.

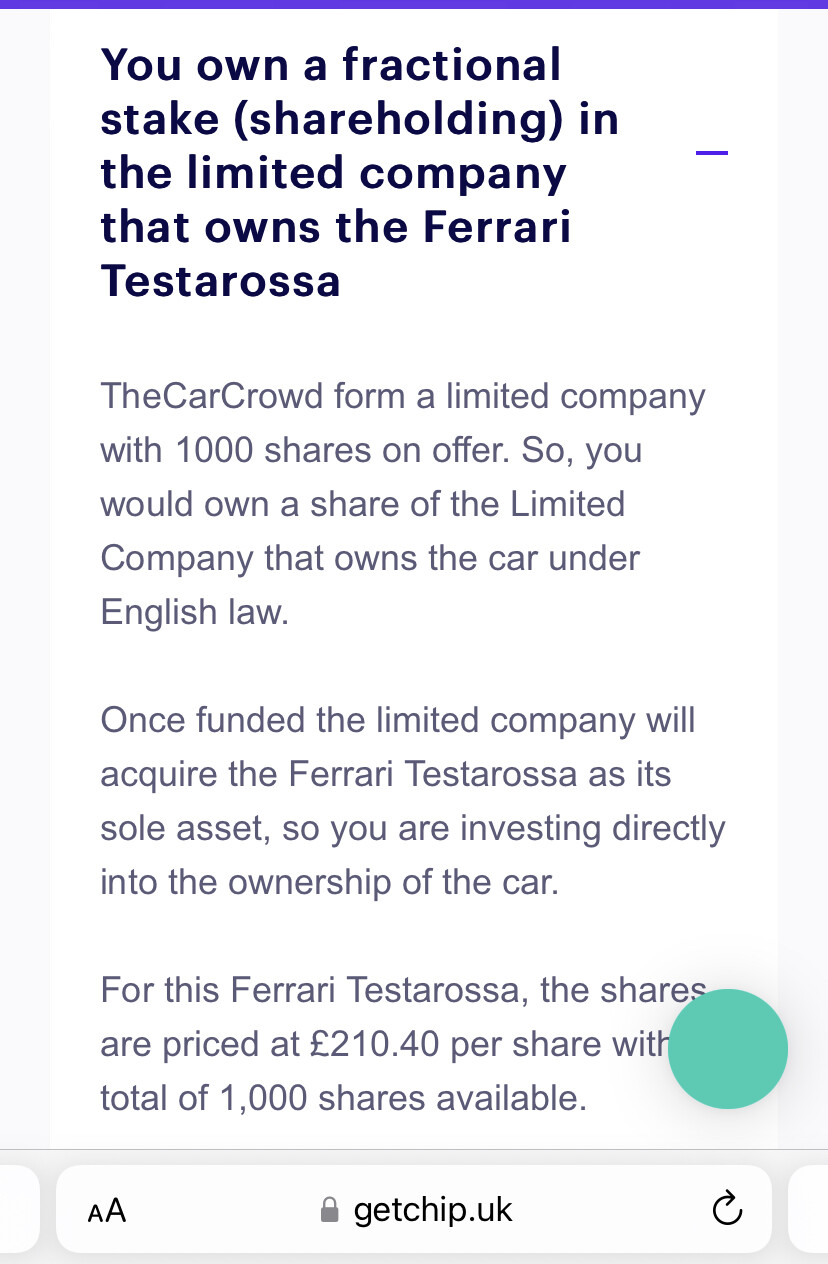

I really don’t get Chip anymore, I’m paying them to invest in a car that someone else will own and drive?

People need to stop investing in this rubbish, now.

(And hopefully the people who work their which are totally blameless I bet for the most part can find work elsewhere soon)

You’ll own the shares of the company that owns the car. The car is kept in storage and isn’t allowed to be driven, but can be rented out e.g. to feature in a film backdrop to earn some yield.

Hopefully Chip doesn’t fail but I just don’t see them raising the VC money they’ve been promising later this year. They’ll do another crowdfund in Sept 22 without a VC secured imho, and I’m just not sure their crowdfunders will buy what they’re selling at that point.

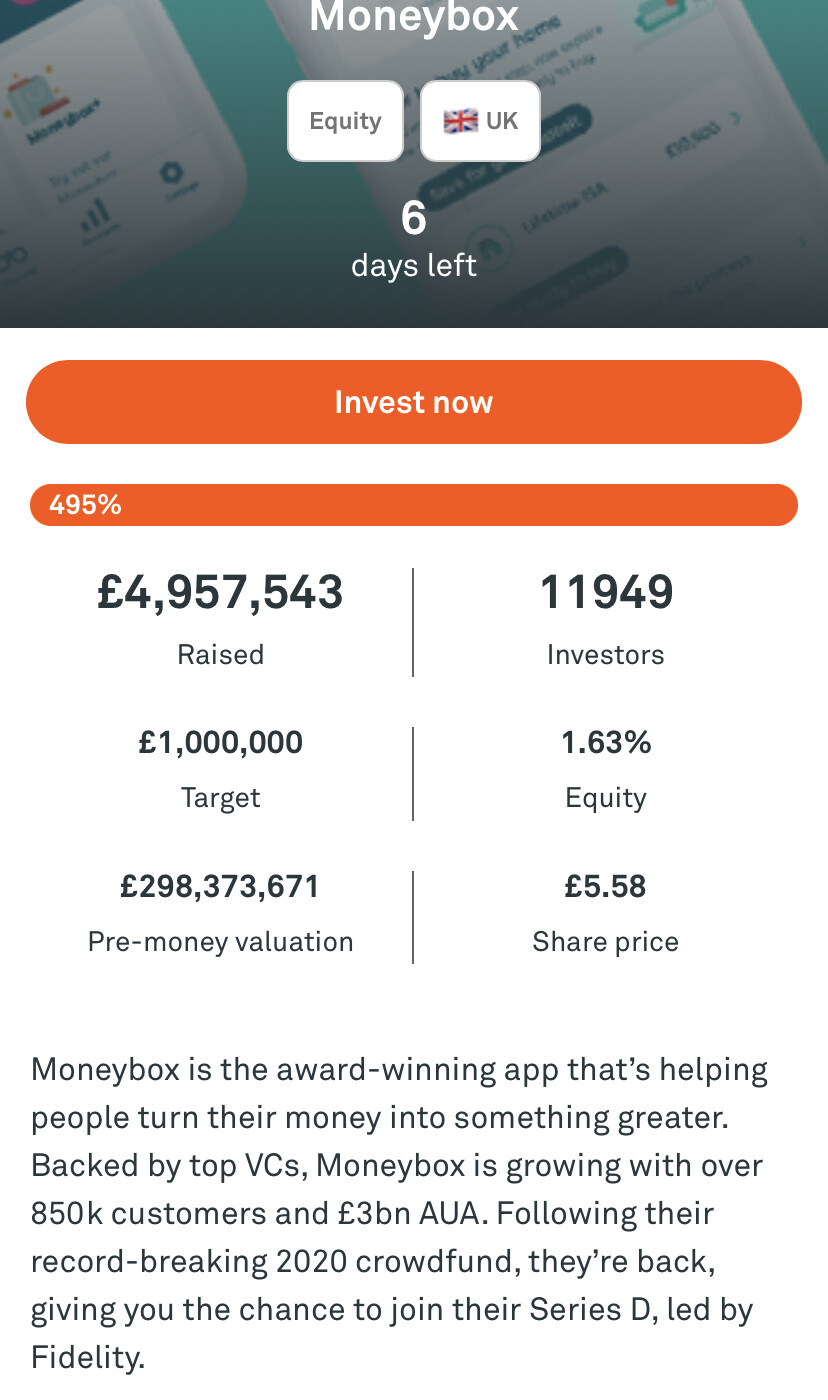

MoneyBox are raising right now on Crowdcube after raising £35m Series D led by Fidelity Strat Ventures. Their business model, roadmap and VC backing is clear which can’t be said for Chip.