Nope - it just treats it as a new transaction paid back to your card.

It’s nice that they’re offering cashback - but it’s definitely the way they’ve implemented it has been ‘cobbled together’ with duct-tape and sticky-back plastic.

It’s not as well implemented as Chase. But it’s ‘free’ (ish) money. And you get more from Algbra per transaction (if on Apple/Google Pay) so I can live with it.

And I have a lot less conflicting ethical issues with Algbra vs Chase.

I chased this myself and had a response Yesterday basically telling me to bear with, but this morning I had loads of cashback show up, so they’ve presumably worked through the backlog.

Not sure I trust them to keep going without another lull though

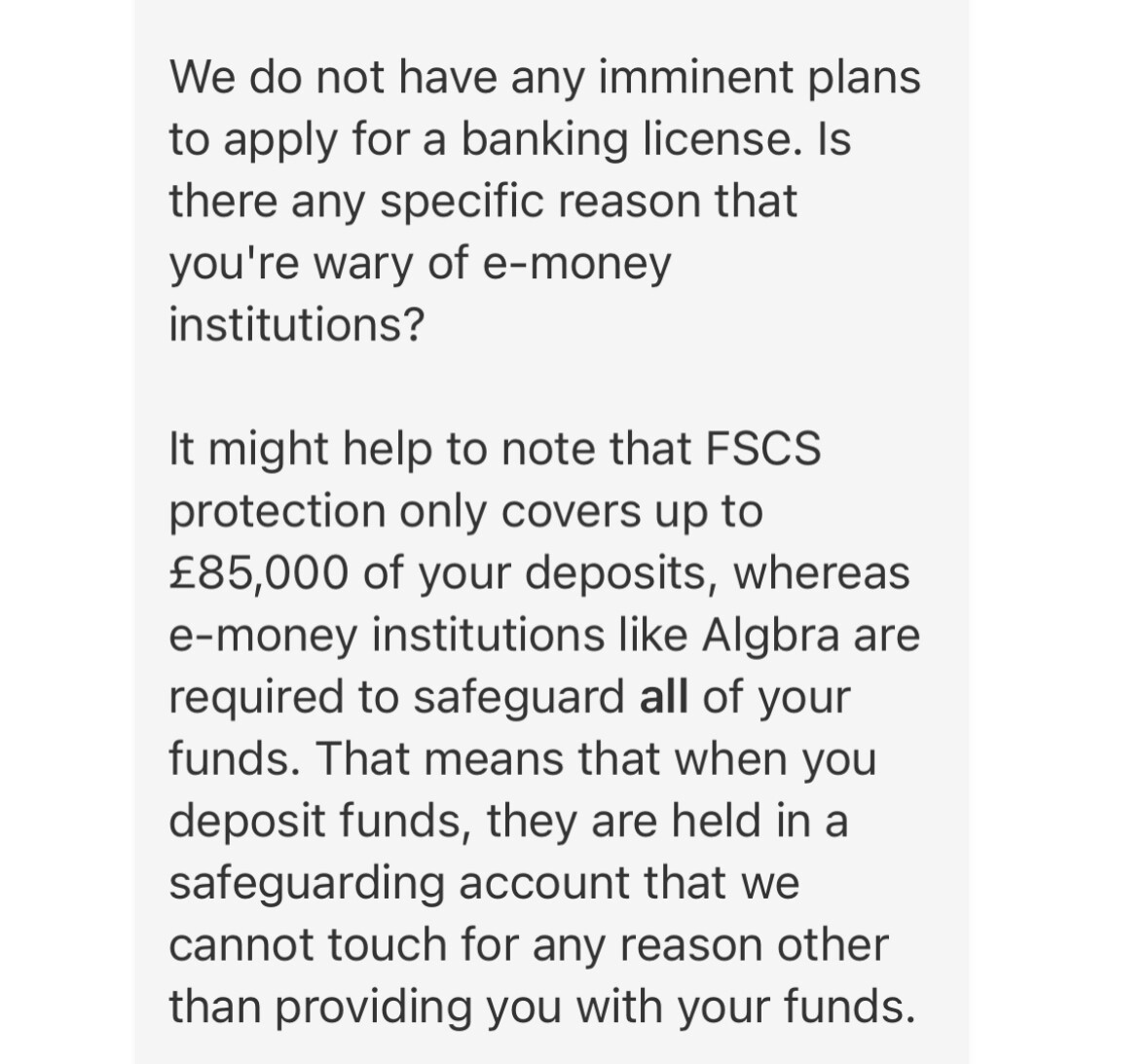

I asked live chat (who were quite responsive I must say) about a few things namely whether they had an intent to become a bank, and connecting to budgeting tools. If they did the latter I’d serious consider them being my return to fintech.

Sadly it was a no and not too sure but I did think the below was a little poorly worded. EMIs (Revolut are similar) really do need to better explain what safeguarding actually is.

The customers I deal with at work (a high street bank, fraud) are generally happy with Revolut.

Generally older folk are more inclined to stick with a high street bank cuz FSCS or ease of service, but it is enlightening to see those who frequent revolut.