Have you read her post? Karma isn’t lending you any money, it’s monzo so the important score is the one monzo gives you.

Yes, you are referring to this part I assume?

If your CK score is high, I can’t think of any reasons your Monzo score would be low.

If you didn’t fit the bill with Monzo, the chances are your CK score isn’t that high.

Edit, although I should add that I wasn’t told I couldn’t get one based on credit score, I was told it was due to income/expense… hence the question about joint accounts.

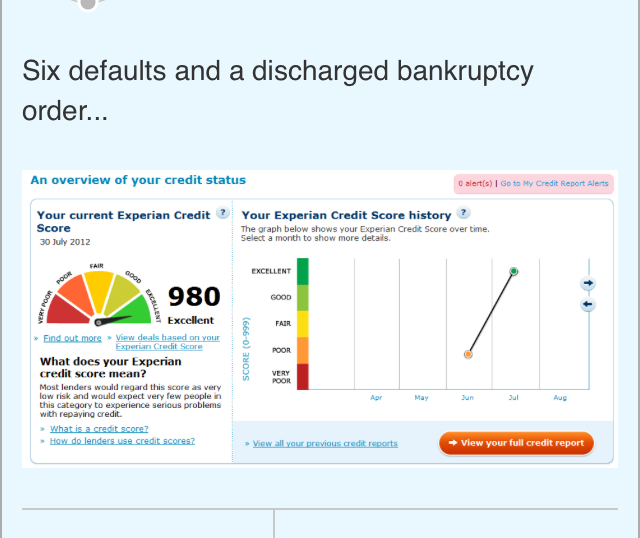

I don’t think the credit reference agency scores are seen by banks that search your credit record. Those scores are just there to give you an idea of how the credit reference agency think you are doing based on what they think might be of interest to a lender.

The banks only see your credit history and then have to make up their own score. That score could be very different if you don’t meet the criteria for the sort of person they want to lend to.

1 Like

Ok, we are moving past my actual point about the JA now.

The only reason I mentioned my CK score was to add a bit more context, but considering my “decline” message focussed on the income/outgoings, I should have just left it out.

1 Like

I’m really disappointed that monzo won’t give me an overdraft or a loan. They are turning into just another bank. I’m desperately trying to improve my credit rating but really struggling. Monzo are just the same as all the other banks

You’re not going to improve your credit rating by going into your overdraft.

Use the features that Monzo have to build some savings, create an emergency pot and use that as your overdraft.  Then when you get an alert that you don’t have enough funds for a payment, you can withdraw from your pot to avoid charges. Both of these will then have a much more positive impact on your score.

Then when you get an alert that you don’t have enough funds for a payment, you can withdraw from your pot to avoid charges. Both of these will then have a much more positive impact on your score.

This is one of the features that makes Monzo not like every other bank - they don’t shaft you with charges at every opportunity

2 Likes

If you want to improve your credit HISTORY, get a credit builder card (aqua, capital one…) and pay it off in full after the statement is issued. But never use your overdraft.

Can anyone answer the question why interest rates on loans seem to drop significantly once the loan amount is 7k or 7.5k in some cases? This seems to be the case with ALL loan providers. Why should a loan of 3k be so much more expensive than 7.5k? I’m genuinely curious what factors cause this

Thank you for taking time to explain the differences. It’s good to get a better understanding of what happens behind the scenes

I don’t have a clue but is it not a case of simple math?

To make it worthwhile to lend a smaller amount they charge more but on a larger loan a lower percentage can still be a lot of money?

I haven’t got an overdraft to go into. I’ve got a credit builder card

I’d agree the actual score you see on credit files doesn’t mean much (it’s a generalisation).

No bank or organisation uses the same criteria to score people. Just because your credit report shows a good score could mean the agency just rank parts of your file differently or are looking for different things.

Banks don’t ask the agency what someone’s score is and use that number. They ask for their file and generate their own score based off that information on a scale or criteria that they have created.

3 Likes

That’s a good thing, you never want to go into your overdraft - nevermind if you’re trying to build your credit score

Since? I had mine since june 2018. After 11 months I could get an Amex and 0% virgin card.

Since jan 2018 it’s gradually getting better

Have you tried to get a prime card? You should be able to get one.

No I haven’t tried I’ll try later

What’s a prime card?

I had a loan with FD when I had my current account with them. They weren’t competitive so I moved to Zopa.

Depending on your circumstances, Zopa is offering cheaper loans than Monzo. They are just as flexible and better value.

I’d recommend people look at the options before diving into Monzo. I don’t see anything about the Monzo proposition that is new, let alone revolutionary, when it comes to loans and they’re not the cheapest.