Mostly likely yes.

My investments are up 14% in 18 months and I trust BlackRock a lot. Only vanguard I tried equally in terms of holding these investments.

And no other index funds I have is close to the 14% in 18 months my Monzo investments have made

Would be great to keep it as it is and really don’t know why Monzo would be changing partners on this

Thanks I searched for investments and sorted by latest and this one didn’t come up for some reason.. appreciate it

This is a September 2023 post tho. I received an email this week saying they are changing partners..

The topic was created in 2023, but it houses all discussion related to Monzo investments up until recently ![]()

1 Like

Thanks

Hello, I had an investment pot a few years ago but closed it down as investing wasn’t a priority. I’m now in a position to invest but I don’t understand why is saying the following?

A few years is a long time ago. Whatever has happened over that period means you no longer meet their criteria.

1 Like

I’ve been seeing the same screen since it launched. Not sure why probably because it’s not my main account or something. I do use the Flex card monthly though…

I used to have an investment with Monzo and I’m still able to make a new investment should I want to. Monzo isn’t my main account, either.

1 Like

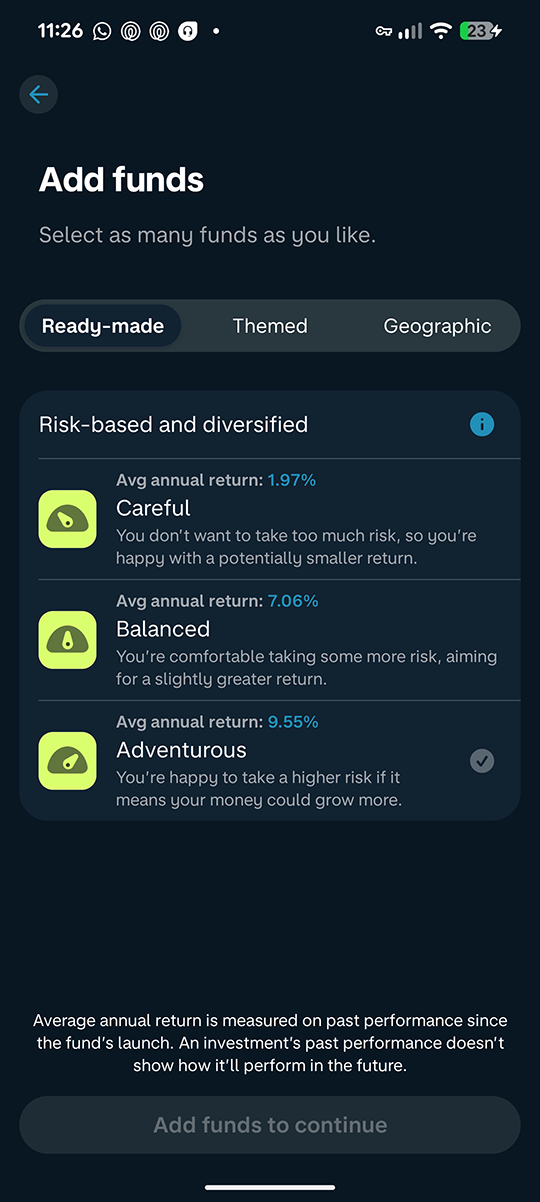

They changed the custodian company. You still investing in Ishares (Blackrock) Monzo investments pots

That’s kinda weird. They are not lending money and it’s invested into an ETF/index fund. Very minimal risk even on their highest risk option. Not sure why Monzo would not allow this. Government is currently trying to motivate people to invest instead of holding everything in savings.

Had an adventurous fund open for a few months. Just moving it to InvestEngine.

Now getting to grips with 212 trading and Invest Engine. Far lower costs and very wide range of options. So easy to rebalance and modify your portofolios.

Aso 212 now have 4.05% interest on any cash either in the ISA or Invest account, (with a debit card also on the Invest).

1 Like

Investments still paused for everyone?

4 Likes

Yep. Not a big deal for me, I add to mine at the start of every month when I get paid.

Hopefully they lift the pause soon though for everyone else

Not for me I don’t think - could still open one if I wanted by the look of it

Yea mine are still paused (and my pension) hopefully the transfer completes today.

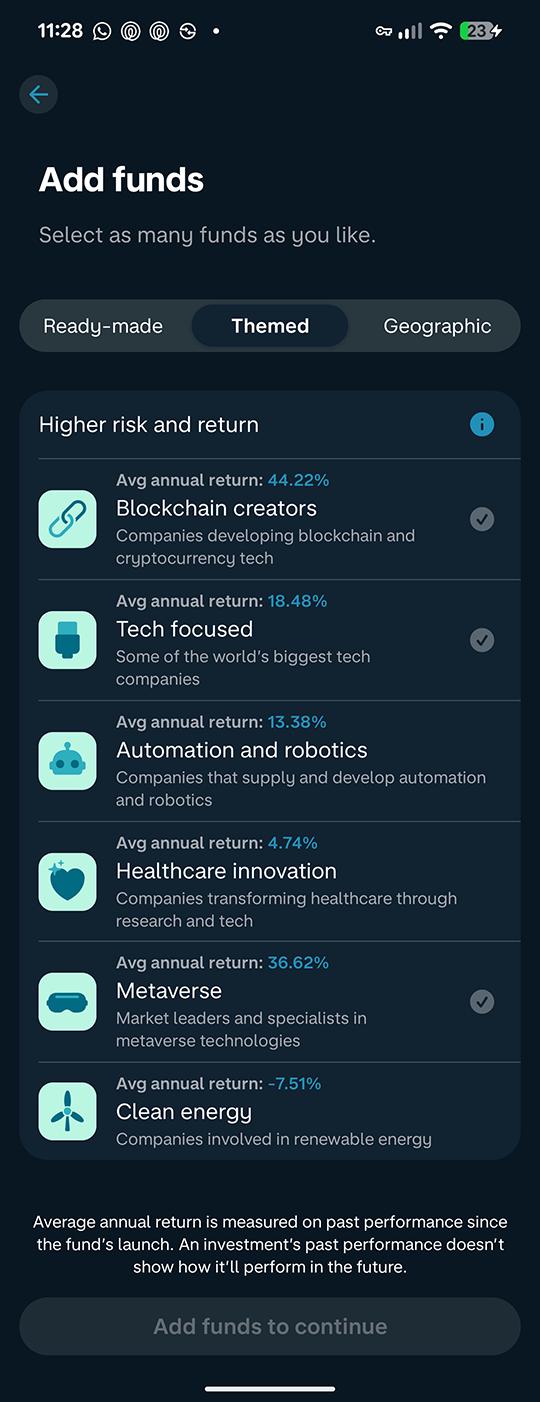

Mine now unpaused - can select the themed/geo funds.

Don’t seem to be able to transfer between funds though - it looks like if you want to transfer some, or all, of the (example) ‘Adventurous’ fund into one of the new themed/geo funds, you have to withdraw from ‘Adventurous’ into your current account first - takes up to 3-4 days - then add funds from your current account to the required themed/geo funds.

Nothing for me just yet, still paused

Did they send a notification?