So an automated process is unfair on Starling to use. Yes I’m sure it’s got a cost attached to it and I’m guessing that cost is tiny in the grand scheme of things.

If this avenue was getting abused they could write easily restrict it, the fact the haven’t suggests it’s not an issue one bit.

I don’t doubt they have a clause like Monzo’s “we can close your account for any reason at two months’ notice” that can be used if they have a problem with any customers doing this.

I sort of love the fact that there seems to be an innate fascination with Starling as the only alternative for cheques. The reality is that many different banks offer the ability to receive cheques more easily and customers may use any of them.

The world really isn’t shaped around Monzo and Starling locked in an eternal battle for cheques.

I don’t think fairness has anything to do with it tbh. They are a business, they offer a service and choose not to charge for it. You use that service. All seems fair and open to me.

I think it’s probably because of all the alternatives, Starling is the easiest one to sign up for and start using right away (other alternatives may insist on a branch visit to prove you identify, say).

I’m sure someone on here opened a Starling account, deposited a cheque in the app straight away, and spent the funds on the virtual card the next day. (And all with just a soft credit search, too, if that’s important to you.)

No other High Street bank can offer that, and for me, that’s a modern-day current account at its finest.

I’ve had a bunch of the duplicate transactions in the last couple of weeks. Usually I’d only get one every few months. Always Tesco. Interesting that it says Tesco aim to refund them within a day - it always takes 8 days.

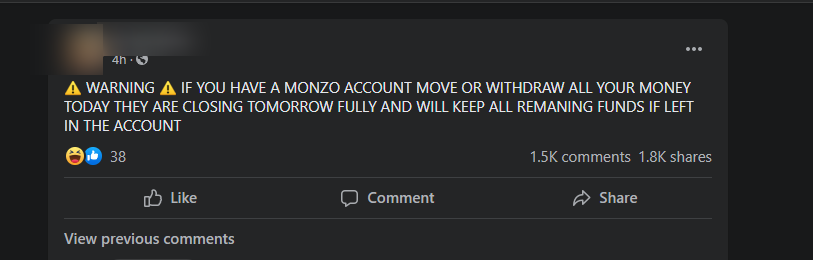

I found something amusing on Facebook this evening. The comments are just loads of people tagging others and so on… Seems like quite a few people actually believe it

)

)