Yes, I got £2 refunded.

I realise now that technically I get Greggs with O2, Octopus and Monzo. Is anyone paying at Greggs now?

Yes, I got £2 refunded.

I realise now that technically I get Greggs with O2, Octopus and Monzo. Is anyone paying at Greggs now?

You’ll get a pro-rata refund, a full charge for the new subscription, and then the fee will come out on the same day you changed over each month (so e.g. if you did it today, you’d pay on the 23rd going forward).

Just to come back on the Railcard eligibility ![]()

If you’re aged 18–30 or 60+ then you’re eligible for one of the age category Railcards.

And if you’re aged between 31 and 59 then there are a range of Railcards available for travelling with friends, partners and family members as well as Railcards for travelling in certain parts of the UK.

So (technically) there is a Railcard available for everyone — but understand it will depend on your needs and circumstances ![]()

Yes! Like yourself, i will probably also switch to Extra, as I only have Plus for the Open Banking really.

That said, i must comment that adding family cover to the Max plan takes it to £9 above Nationwide’s FlexPlus for essentially the same benefits (Gregs and Railcard are useless to me), so no one who doesn’t care about Greggs and Railcards would really choose Max over FlexPlus.

Are Nationwide running theirs at a loss or is Monzo getting fleeced on their deals with the insurance providers?

The dirty secret is that the cost to Nationwide of breakdown cover, travel insurance and mobile phone insurance bought in bulk is pretty minimal and Nationwide are simply passing that saving along to the customer.

FlexPlus is obscenely good value as a result.

Very much whelmed.

@rossmonzo people from northern ireland cannot use a trainline season ticket. Would have been nice if you worked with translink (ni alternative) to provide something instead

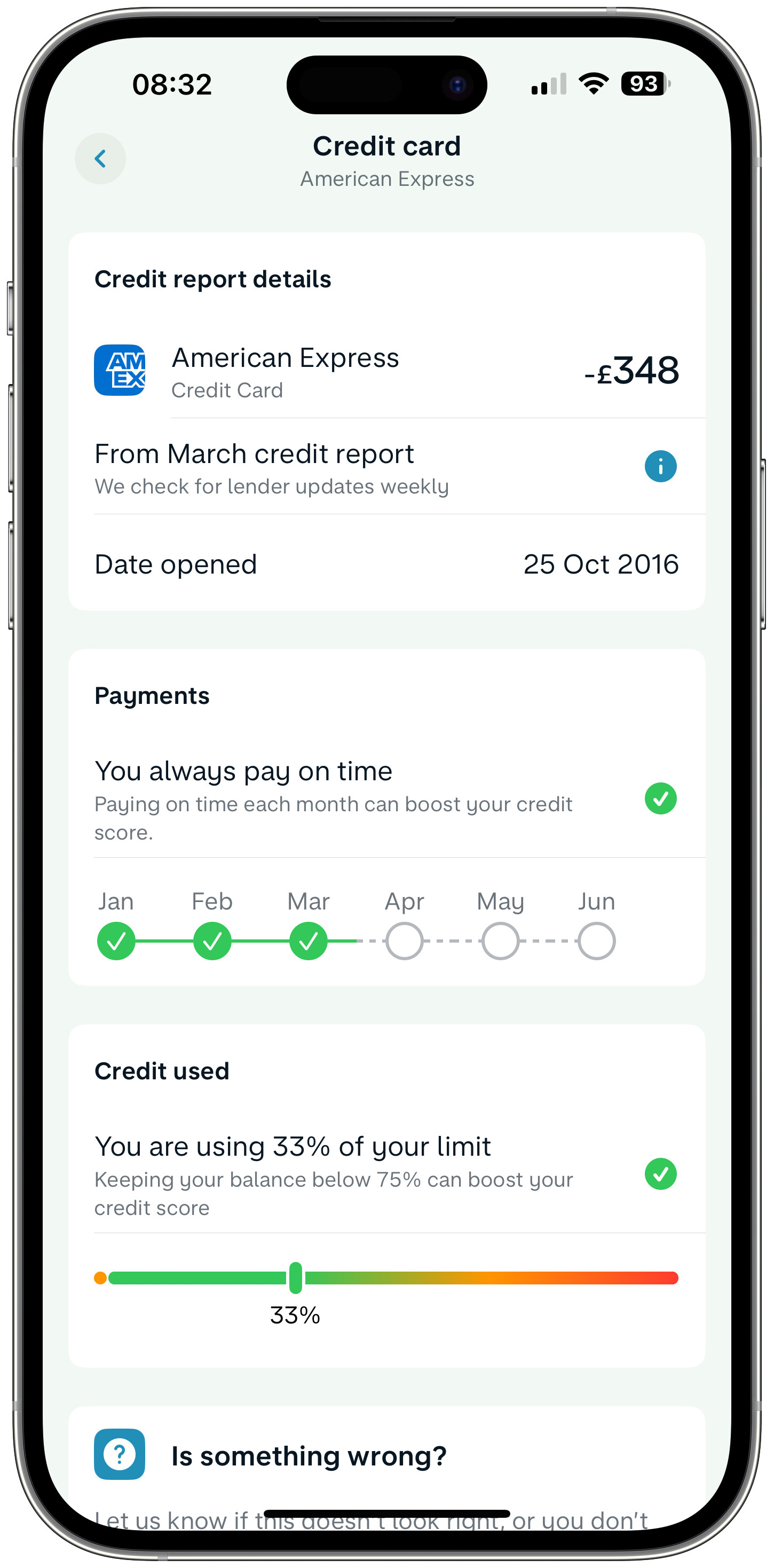

On the credit insights it’s a nice clear layout which I appreciate:

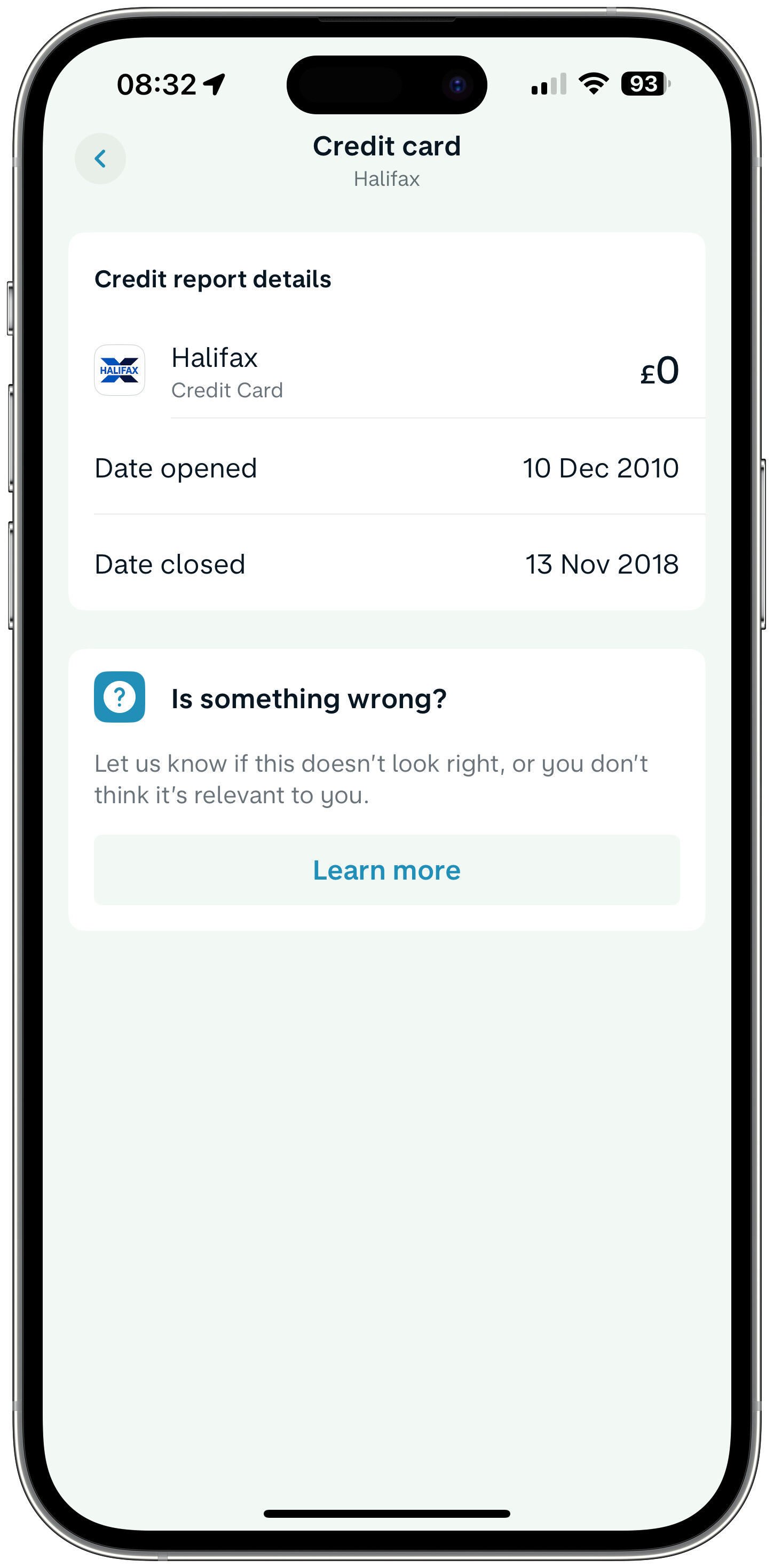

Even the closed accounts is clear and easy to get the opened and closed dates:

What makes it under 30? The railcard? That is available in various other guises so you don’t have to be 29?

Obvs there will be some people that don’t fit for any card, but that’s life.

I really doubt there’s anyone over the age of, really about 25, who genuinely thinks a sausage roll is going to be a factor in their choice of financial product.

That perk is honestly more baffling to me the more I think about it. Leaving aside that we have an obesity problem in the country, how much value do Monzo really think that adds?

I’m a bit gutted about the loss of discounted airport lounges, that was a real draw for me. Sad to lose the metal card too but very happy it’s no longer white and easily stainable!

I’m going to have to consider whether this works for me or just stick with Premium.

You can get a coffee ![]()

Let’s say £2.40 a week saved, that’s still £115.20 saved if you buy a coffee a day (which isn’t unheard of).

Of all the issues, national obesity isn’t the one with these plans.

Its loss of Cashback on international transfers… not cashback on spending at UK retailers

My mistake, I edited my post when I realised! Well that’s something at least!..

@rossmonzo Just tried sharing the blog post to someone who isn’t on the forum and it doesn’t come across very well.

Honestly, I’m a little bit disappointed with the lack of “Premium” features on the highest tier plan, along with the increase in price. I used the airport lounge access regurally, and at the price range it’s getting very close to competitors like Revolut who’s Metal plan seems more-right for me now at £14.99 a month, and the Nationwide FlexPlus account, atleast in terms of family insurance, seems like better value

Like some others said I already get Greggs from O2, Octopus, etc

Credit tracker is nice but it gives the same data as Credit Karma which is free, locking it behind a paypal feels a bit eh; but I guess there’s some API costs that you guys probably need to balance out

My question: Why Monzo Max + Family addon, instead of FlexPlus and Revolut Metal?

A couple of queries about Max. Monzo’s own documentation etc., stipulates an age range of 18 - 69.

Does this mean that when hitting the age of 69, access to Max just stops completely?

Or is it intended to be the Upper Age Limit for the Travel Insurance Product.

When I click through into Zurich’s T & Cs and Product Information I find this:

The maximum age limit for all benefits is 70 years inclusive. When you reach the age of 71, cover will continue until the next anniversary of your Monzo Individual plan but not thereafter.

I don’t think I’m missing anything blindingly obvious but this doesn’t seem to match Monzo’s 18 - 69?

I’d be really grateful if someone could clarify.

TIA

I’m going down to Extra I think.

The two things I care about (export/categories) are there. If I used Greggs then that’s a decent offer but I don’t, the only time I’ve been is on a UK break! So not going to use it week to week. I’ve never used the offer with Octopus. Increased interest, I can already better, granted not instant access, but I don’t have to pay for it. I’ve never paid cash in. I don’t invest enough to worry about fees and I’ll just move it all elsewhere. Railcard, not worth £4 a month when it’s £30 a year when I can buy it outright, if I need it.

I don’t think there’s a big enough hook in Perks to get me to pay extra, which I would have willingly, but you’ve kept enough in Extra for me to be happy to downgrade. Which was always the danger of having a cheaper plan!

For £13 a month I have Nationwide flexi plus. For that you get Travel insurance and mobile phone insurance FOR THE FAMILY and UK & European breakdown cover.

I’m a full time Monzo plus customer and have been for year and love Monzo, but the price of these plans just aren’t appealing enough compared to others out there.

Does anyone know how the railcard works if it is kept in the Trainline app? Are you then forced to use the Trainline app to book tickets?