From a consumer point of view, unless you’re a baller, then I don’t think the cashback is better. But it’s easier and no hoops to jump though.

It’s undoubtedly better for Chase though.

From a consumer point of view, unless you’re a baller, then I don’t think the cashback is better. But it’s easier and no hoops to jump though.

It’s undoubtedly better for Chase though.

Personally it sounds better, because if someone gives me £150 I can think how to spend that in pretty much a couple of transactions.

1% cashback for a whole year makes you think how much could I get back, feels like you’re earning on everything and generally unless you do the maths you don’t realise you’re unlikely to get the same amount as a bonus.

If I had to say how most people think, a sustained cashback over a year sounds like a better thing to have than a one off lump sum.

I understand your reasoning, psychologically speaking, but I don’t really agree.

I think most people can quickly work out 1% in their head, and realise that they need to spend £100 to get £1 back.

I agree with @Revels, who basically said what I was trying to say in a more blunt way!

What it will do, for Chase, is persuade me to actually use the account as my primary spending card. That’s smart as if they just offered a bonus I would likely bag that and keep the account to see what happened long term but not really use it (spending, generally, on cashback credit cards instead).

Everyone is different!

But you’re right, it’s far better for Chase as a bank. I’m surprised nobody else has done this before. You could even offer a much higher cashback for a year if you switch, forces the customer to use the account to obtain the cashback and is more likely to have longer term customers.

I can’t do the maths but let’s say £150 over a year, that’s 41p a day. Even if they offered 5% cashback, would most people make that every day over a year?

TSB did something like it a while back, I think they gave you 5% back for using Apple Pay (for up to £5 a month back) on your Classic Plus account for a year.

They also did a credit card offer which was 1% back, that also ran for around a year (possibly longer) and the cashback was paid monthly.

It’s wasn’t quite the same as Chase, which is very Apple Card-esque, but the concept has been tried. You are right that everybody’s different, but it didn’t seem to attract a huge number of new customers for TSB.

TSB offer £5 a month back after 30 transactions at present on their free spend and save account. 6 months only though.

I think having a cap ruins it. Although you’re right in that you’re really unlikely to ever make the £150 in a year the concept that you technically could and more is the fun part.

If you cap it then it loses its appeal to me. Or at least cap it at a higher amount that is about the amount £150 would be.

Maybe just read what is in front of you instead of asking all the random questions to customer support causing contradiction.

It’s clear from the website from date of activation so I don’t understand why you then need to ask the live chat about the information you have just read and accepted or OK’d.

As someone else mentioned, attempting to go to multiple people you’re more inclined to get a different answer instead of using common sense to understand the words right in front of you.

Seems like you’re just out to try and catch Chase out for bad service or similar.

Probably wise; and less frustrating or entertaining for you, to make your own interpretation of the facts given before applying for things and go from there.

Yes, it does really, especially given your point about the “idea” that you could earn thousands in cashback having an allure!

It’s not clear from the app itself, and it should be.

That’s the point I was making in my (constructive) criticism. It’s not completely clear from the website as the website refers to “activating” the cashback; the app activates it when you click OK (but it is not 100% clear that this is what is happening when you press OK).

Well, it’s free money that comes with a free account.

I know!

It’s worth having, I don’t disagree, but they should make minor changes to the app to make it clear that you are switching it on in my humble opinion.

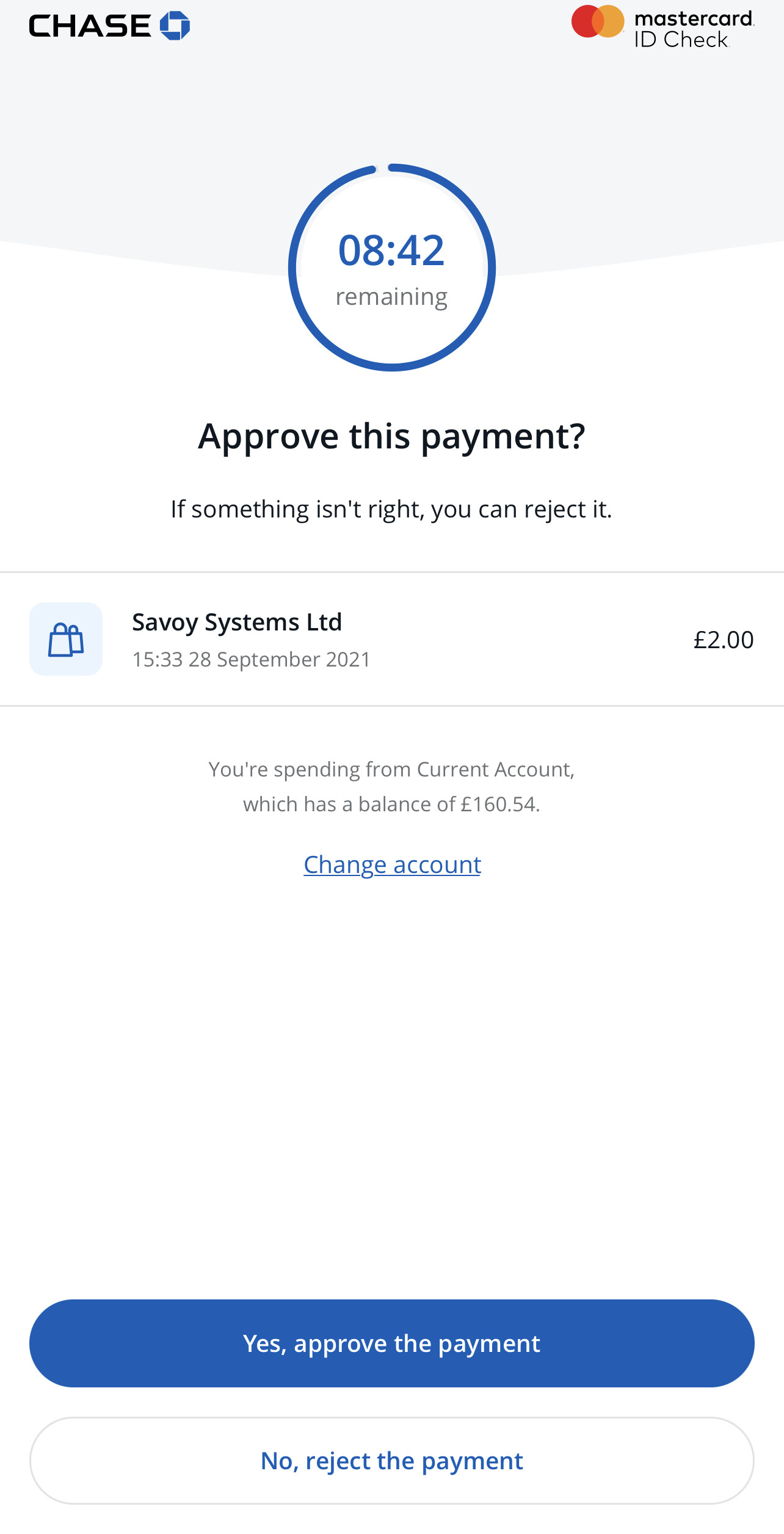

Not sure if this has been pointed out but when you make an online payment you can change the account the funds come from while authorising:

Yeah I noticed this as well

I’ve literally already explained above what I was unsure about and why, despite reading the information that was available to me, so I won’t bother again. At no point did I go to different people to try and get a different answer or to try to ‘catch them out.’

Yep, I saw this the other day. A nice touch I thought!

It’s not a question I’d have asked but, equally, if it’s so straightforward, support really should do a better job of answering the question.

I had no problem understanding it.

Not sure how they could simplify the wording personally but hey ho.

That’s very cool!

Having set this up, they’re missing a trick not offering something like Curve’s go back in time

The difference between Curve’s go back in time and this though is that the Curve system lets you literally pay for something on a different card with a different organisation. You can’t transfer £40 from one credit card to another because you accidentally used the wrong one.

With Chase, if you paid for something out of the wrong account/pot/space/whatever they’re calling them, you can then just go and transfer the money yourself back in from the correct pot and sort it out.