Hi everyone

Thanks for your comments and feedback! I’m one of the people involved in building cash deposits - I’d like to confirm a few things people have been speculating about and some details that we haven’t announced yet.

- That is indeed a blurred out PayPoint logo. All of our contracts are now finalised so we can announce we’ll be partnering with them on cash deposits.

- This should be live in a few weeks. We should have a solid launch date to announce next week.

- We are planning on charging £1 per deposit (if you hand over £40 then £39 arrives in your account).

- There’s a minimum deposit amount of £5 (you must hand over £5 or more).

- There’s a maximum per-deposit limit of £300 (you can’t hand over more than £300).

- And there’s a cumulative limit of £1,000 deposited over 180 days (approx 6 months).

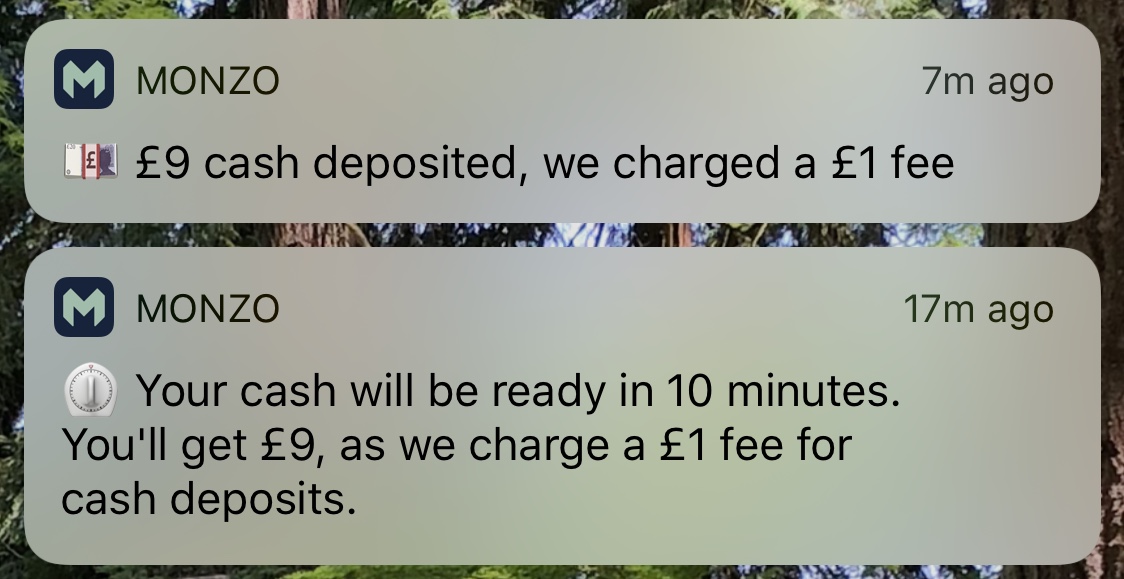

- You’ll receive the money in your account after 10 minutes. Once you’ve handed over your cash and the shopkeeper has given you a receipt the money will arrive in your account after 10 minutes. That’ll look something like this:

Having read through this thread, I’d like to offer some insight into how we’ve made these decisions.

Why PayPoint and not the Post Office?

I mention this first, as the answer to this gives some important context for later points. Essentially, it was a better option in almost every regard.

One major blocker for the Post Office is that it will require us to update our chip profile – a change that we can only do by physically replacing everybody’s cards.

PayPoint have approximately 29k locations spread across the UK. Even the village in Scotland where I grew up has one! I learned where the Scilly isles were the other day when I used our internal merchant tool to plot all the locations (see below), and zoomed in on a mysterious dot in the sea. There are far more PayPoints than there are Post Offices, and the convenience stores hosting them are often open late.

Your milage may vary on this point, but in my experience using a PayPoint would be far more convenient than a Post Office – there’s one in a little shop that I walk past on the way to work every day, which is open far later than the Post Office is. I’m unlikely to have to wait to be served, and I’m probably in there a couple of times a week anyway.

We aren’t ruling out the Post Office forever – we’re likely to eventually incorporate both the Post Office and PayPoint.

Why are we charging?

As some people pointed out, lots of other banks don’t charge a fee for depositing cash. They usually do this by making up the money elsewhere instead. But we don’t think it’s right to ask everyone to subsidise a feature which we only expect some people to use.

We could try to absorb the cost ourselves, but we don’t think that’s sustainable for us as a business. We’ve just raised money and we’re working hard to become profitable on a unit economic basis, then overall. So we don’t want to add extra costs that scale with customers.

You should launch this for free and then charge if you have to / Launching this with the fee from day one is likely to give you skewed usage statistics

We didn’t want to launch cash deposits for free, then introduce a fee if we needed to. When we’ve done this in the past (like with cash withdrawals abroad) we’ve found it can be confusing for customers and feel unfair.

Instead, we’ll regularly review how people are using the feature, and work out whether we can reduce or remove the fee. The fee for cash deposits isn’t set in stone, and we’re definitely not ruling out the possibility of making them free in future.

Launching this with a fee will change the usage pattern when compared to free deposits. That’s unavoidable, but having some data is better than having no data. If we’re unhappy with the quality of the conclusions we draw from the data in a few months time, then we can run some different trials / experiments and compare the datasets.

Make the first one free / Make it work like international ATM withdrawal fees

We explored this option, but ruled it out as we couldn’t make the numbers work. We built a model comparing different “first one’s free” approaches, but for each one you’d need a significant number of people depositing cash at least once a week in order to balance out the cost of the “free” deposit. Again, we thought it would be fairer to pass on the costs to everyone who uses the feature, than only charge the group of customers who use it more than once.

We populated this model with data from a survey we conducted several months ago. It gave us some idea of how often people want to deposit cash, and how much. It didn’t take into account the convenience factor of using PayPoint (i.e. you’re more likely to do it because it’s right there, vs going to a bank branch).

A “first one’s free” approach is also complicated to explain and understand. Our customer support team fields about 10 questions a day about how international ATM fees work. A free cash deposit in a given period is probably easier to explain than ATM fees, but in our experience conveying information like that succinctly and correctly is difficult.

I wouldn’t use this to pay in small amounts of change because of the charge

The convenience of PayPoint would naturally lead to people making more cash deposits through Monzo, compared with how many they do with their bricks-and-mortar bank right now. For many people it’d be so much easier to deposit amounts they wouldn’t have bothered with before. Without the fee, I would personally be quite likely to deposit money to get rid of change if I was in my local corner shop.

Unfortunately, we can’t absorb the cost of this kind of usage. Peter’s post earlier was absolutely on the nose about this.

£1 is expensive for individuals with lower income / It doesn’t work well for people who rely on cash / This isn’t “making money work for everyone”

We’re adding a feature which we previously weren’t able to offer. As a result, some people will be able to get more out of Monzo than they could before, which we hope makes their money work better for them.

As I’ve said above – we’ll review the fee once we have more data. Making money work for everyone is an ongoing process!

Monzo is charging people for putting money into their account, money Monzo will then profit from

We would earn money on these deposits through two channels:

- Interest earned from the Bank of England. This is interest Monzo earn on the money if you leave it in your account (currently set at 0.75% APR).

- Interchange. This is an amount of money Monzo get paid by Mastercard whenever you use your card (0.2% transaction amount)

Assuming we made cash deposits free, if you were to deposit £100 in cash and leave it in your account it would take more than a year for Monzo to make back the cost of the deposit. If you were to deposit £100 and then immediately spend it we would make a loss. In fact, it’s impossible for us to break even using interchange alone – if you spend £300 via a normal debit card purchase we would earn 60p. We would just about break even on a free £300 deposit if it stayed in the account for two months and you then spent it as part of a normal card payment.

Why are the limits so low?

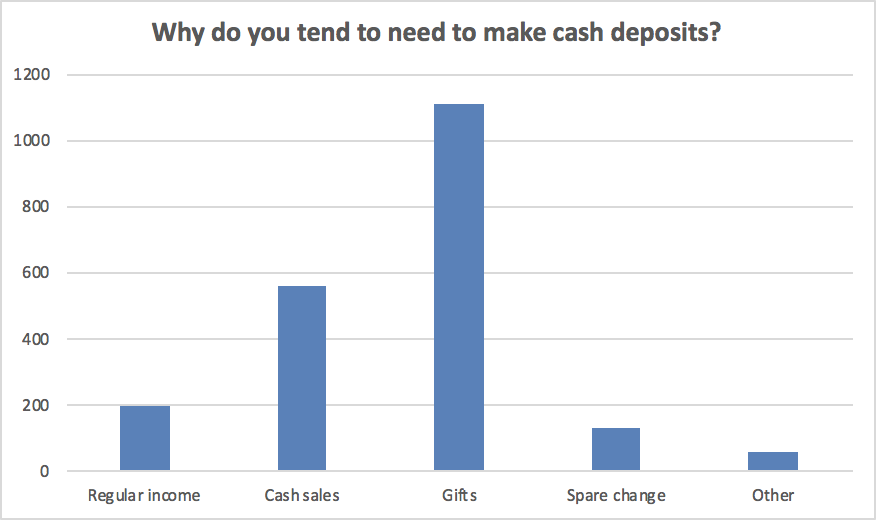

Cash deposits represent a very high risk of money laundering. A number of details of our implementation with PayPoint mitigate this, but from the result of our surveys indicated that a limit of £1,000 over six months would cover the vast majority of use cases.

The responses to our survey question “Why do you tend to need to make cash deposits?” had the clear winner of “gifts”, with “cash sales” coming up in second place with half the votes. We especially want to cater to the first use case, and think these limits should work for most people.

Again, we’ll review these limits once we have more data on how people use the feature.