The card not arriving here yet may well not be their fault. There are several points of friction in the delivery process. It may even have been stolen.

So yes, I am impressed with their Customer Services Team.

One of the measures of a good company is how well they respond to things not going to plan - T212 have responded very efficiently here.

A follow-up to my posts 2 and 4 messages upthread re T212 Customer Services.

I cancelled the non-arrived card in-app mid-afternoon on Friday( 3rd) and emailed back to the address I had been given to set in motion the refund process. I got a courteous reply.

Later that day, I received an email outlining what would happen next and asking me to be patient. Fair enough.

Just before 10 am today (Monday May 6th) I received an email informing me that my refund had been credited to my account. A quick check in the app and yes, the money had been refunded already.

So, essentially, from starting the process mid-to late afternoon on one day, the money was refunded to me before 10 am the next working day.

This is exceptional Customer Service by any standards.

My trading212 says 1.5% cashback until October. Is this a thing or typo? And the cashback seems to be daily so a bit hard to confirm the rate at a glance.

Also in my limited one off test converting during market hours versus spending on MasterCard out of hours yielded 0.4% better rate with Trading212. Which may be offset with credit card cashback, or credit card interest free period a bit.

True, although think the primary idea is more offering a full personal wealth service suite to clients across Spend (Card), Save (Cash ISA) and Invest (S&S ISA and SIPP long in the works) so that you don’t really to leave their ecosystem if you don’t want to.

HMRC have recently updated the Flexible ISA rules so that you can now only repay withdrawn funds into the same Flexible ISA that you with withdrew them from.

No more withdrawing from one Flexible ISA and repaying into another.

They updated the guidance for ISA providers on the 30th April. It’s completely ruined my plan for drip-feeding my S&S ISA from a flexible easy-access cash ISA.

“30 April 2024 The ‘flexible ISAs’ section has been updated to clarify that, when replacing ISA funds from the current or previous tax year, they must be put back into the account they were withdrawn from.”

That might well be the expectation, but I wonder what processes they may have in place to police this.

There will be many who do not read the regulations who will mix and match as they see fit.

Edited to add: From a budgeting point of view, I guess this favours something like the Zopa ISA in some ways, as you pay into one general account but can then sub-divide into pots and transfer between pots quite easily.

Pretty sure that they just rely on the ISA provider reporting your usage at the end of the tax year. In my case, if all three of my ISA providers report my subscriptions for this year, it will add up to £21,000 because I already withdrew £1,000 from my flexible cash ISA and paid it into my S&S ISA.

I think they’ll be pretty lenient this tax year for any flexible ISA transgressions, given that we’ve been allowed to withdraw from one and pay it back into another for the past few years.

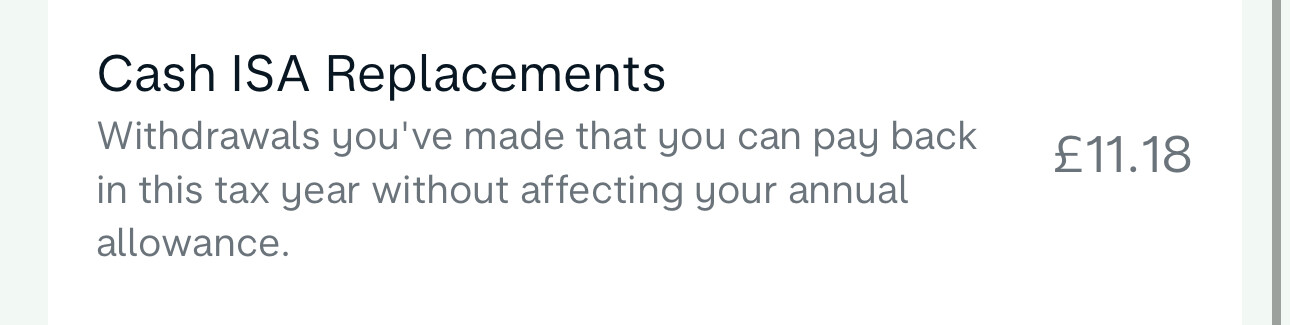

On this, I’ve contributed and withdrawn from my Monzo Cash ISA, but the app only shows current utilization. I am assuming that according to the new regulation they should show current and max if those two are different?

I’ve asked support to clarify this, as it appears Monzo considers the 30th April guidance to have only taken effect from that date, which would be good for me as I withdrew a lot more before the 30th.

It looks like the actual ISA legislation was changed before the start of the tax year and HMRC then realised that their guidance was out of date, updating it on the 30th April.

There’s still a worked example on their website that says that you can pay a flexible ISA withdrawal back into any ISA account!

Not necessarily. It depends on how they structure the ISA. I’m thinking something like the way Hargreaves Lansdowne do their cash ISA which let you put the money in multiple ISAs even before the rules changed.