I think you are correct on both counts. Generally, where the banks have managed to charge a monthly fee in the UK there is a perception of service and exclusivity that probably doesn’t currently exist with Monzo.

@Feathers I think that Monzo has the model wrong - the appeal is in being able to track contactless payments instantly. The established banks can receive my salary, pay my bills, provide joint accounts and statements. Where Monzo excels is in my ‘cash’ spending in a modern world i.e. contactless. Would I be prepared to pay for this service? No, because I can already track it in my existing bank account albeit delayed. The vision by the founders is to suggest/introduce third parties with mutually beneficial services based on account behaviour. The snag as I see it is that the majority will use Monzo as a spending account and very few will pay their bills through it.

I would leave if they introduced a monthly cost for the account. My legacy account does not charge and I would not expect a “challenger” to charge, even with features like instant notifications etc

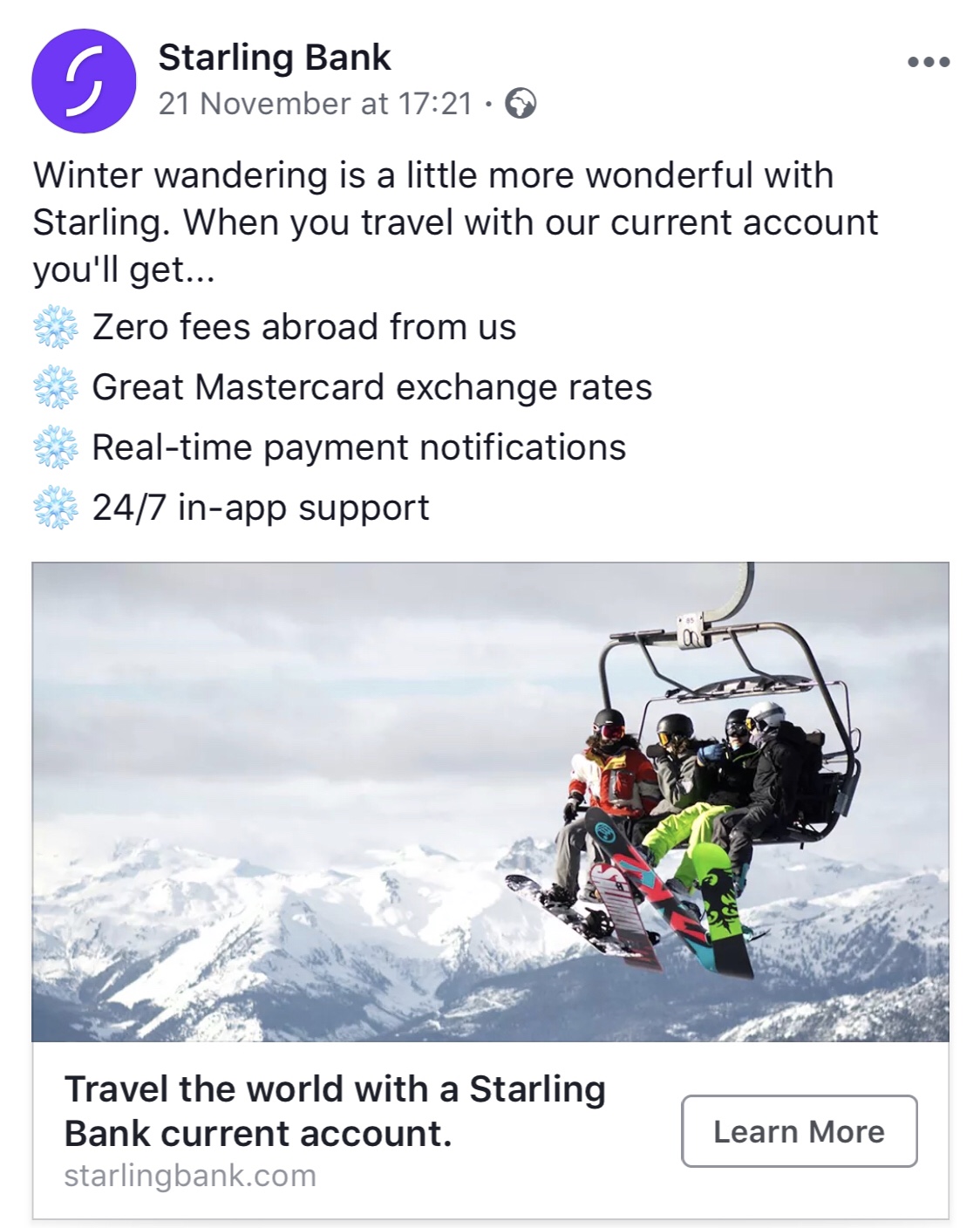

Maybe, but after the introduction of inflated charges to withdraw cash abroad and now a charge for this they are likely to lose more customers to Starling et al. Competitor banks must be grinning ear to ear as we recruit customers for them.

There is nothing wrong with charging for top ups and cash withdrawals etc, but they have been poorly managed. Either Monzo take a business decision to free banking or to charge, and if they take the charging route decide if separate one off charges for everything or one monthly charge.

Monzo need to bring in all potential charges now, be it for Monzo.me or whatever. Another repeat of providing something free and then backtracking and bringing in a charge and appearing if it was bait and switch (even if it was just poor business sense rather than intentional) will just leave a sour taste, and a poor reputation for Monzo for repeating that tactic.

I, like most here, appreciate being asked what I prefer from monzo. But have monzo also considered that most behavioural economists these days do not believe that users always behave as rational economic actors. What they mean is that people often don’t choose what would make them better off or even what they will use. They choose what appeals in the moment, but when it comes to the crunch they actually prefer something different.

In ‘stumbling on happiness’, Gilbert points out that we are terrible at predicting what will make us happy. Jobs is famous for making decisions that most thought were mad, but his genious was that he knew what people wanted.

What am I trying to say? Well sometimes you need someone with vision to make the choice rather than crowdsource an emotional reaction.

Lets talk about this then because that’s a very, very long way off. In the meantime, funding this much of a cost from Monzo’s revenue stream means it can’t invest, which means it can’t grow, which means it can’t attract investors, which means they go bust.

That’s why they’ve given us specific options & criteria for their solution, rather than just asking for suggestions they know what they need to achieve & there’s several ways that they can reach that outcome. I’m sure you’re aware of the benefits of taking this approach too so now, they should get the best of both worlds.

You miss the point. Even when given a restricted set of choices, people often choose something in the moment that they later regret.

It’s only at the point of use that they make the actual choice that makes them happy. Instead of voting, people should be given the real choices in app. Then the choice made will really reflect what they want.

I’m not convinced that’s true anymore in regards to CA. The starling app has between 50k - 100k download badge on the Android Store and is ranked higher (now) in the apple store. I wish they would say, but I do wonder why these fee conversations aren’t coming up there yet.

The problem is that what was decided by users requires quite a few assumptions to end up working for Monzo. For example, regarding overseas cash withdrawals:

If people withdraw under £200 every rolling month, this will be still costing Monzo some money that will be non-recoverable under the current fee scheme.

If people need to withdraw significantly more that £200, it’s easy to split their withdrawals in between Monzo, Revolut and Starling to benefit from the free tiers that all offer (assuming that Starling will introduce limits at some point). This will also make their withdrawal costs non-recoverable.

What was voted by people is only viable in the case where users withdraw enough in aggregate to support all withdrawals.

That’s correct. But I don’t see why that’s a problem? Every business has to model different scenarios when trying to figure out the cost of new pricing models. Sometimes they’re right & sometimes they’re wrong but that’s unavoidable.

Maybe they are coming up internally, but just haven’t been discussed publicly yet. Starling tend to be far less transparent about these things. Alternatively, it may be that these costs are just less of an issue for Starling - Starling never launched a prepaid card, so users never got used to using it as such. I would expect that a higher proportion of Starling users are already using it more like a normal current account, with foreign ATMs and debit card top ups only a small proportion of use cases. For a long time, debit card was the only timely method of topping up a Monzo account, so it’s not surprising that it got high usage and thus high costs.

This is unlikely though, Starling are being charged just as much by foreign ATM operators for cash withdrawals as Monzo & are actively marketing their service as a travel solution.

I’m not sure whether that’s a factor. Either way, they’re using GPS which is the same processor that Monzo used for the prepaid cards & incurred their costs with - Monzo hadn’t rolled out the CAs to a significant number of users when they started the consultation about adding fees & explained the costs. So I can’t see how that would be saving Starling money.