Money paid to and from your account must be from a UK current account in your name.

I already have my savings in a savings account; I’m not happy that I’d have to transfer it to a current account and then into Marcus. ![]()

Money paid to and from your account must be from a UK current account in your name.

I already have my savings in a savings account; I’m not happy that I’d have to transfer it to a current account and then into Marcus. ![]()

That is the standard way of doing things or a disconnected account isn’t It? What else would you expect?

I can select any account with a sort code and account number as my “nominated account” with my current provider.

I’m also curious as to how Monzo or any other bank would see a large amount of money appearing in a current account then going out quickly. I’d be worried that the transaction would falsely be flagged.

I guess from Goldman’s side, for KYC and anti-fraud reasons, verifying you own the depositing account is easier with a current account as it appears on your credit report. Even if Monzo does false flag, although I’ve sent random £4,000+ through Monzo between savings accounts, you should be able to verify ownership very quickly.

I opened an account this morning and may start to transfer my non-LISA savings over.

Anyone know if joint accounts are available and if so how to open one?

Answering my own question. I have just spoken to their CS and the answer is no - it is a sole account. Shame for me as the interest is good.

I have a decent amount of money left over from a remortgage that I was waiting to put into a joint Monzo pot with interest (when they launched it), but looks like now GS will be getting my dosh. If Monzo had pots paying something like this i.e. 1.2% I could be persuaded to put it there as the convenience of all the cash in one place is worth it in my view.

Interested to see how this all plays out!

Have opened an account, my bonus on my tesco savings was about to expire, so good timing!

Made a payment from monzo to Marcus, but it’s not exactly faster at the moment

The holy grail would be a ‘Marcus’ Pot. Especially as they aren’t competing (yet) in the current account space.

This represents a vision of what an OpenBanking future could look like, with Monzo operating as ‘narrow bank’, then leveraging the power of big balance sheet banks (HSBC, RBS, etc) who effectively become back office product providers.

Side thought, wouldn’t it be interesting if Starling became Marcus?

I signed up and it took 5 minutes, super easy. I like that it’s instant access, I’m saving up for a house move and a holiday this year so I’ll put that over there until Monzo open up their offering. Reminds me a lot of ING back when it first opened years ago

Yep it looks very clean.

Takes about 5-10 mins for faster payments from monzo. Similar to Tesco, not sure why it isn’t instant, but not really an issue until we get interest paid by the second

Yeah I was a bit worried I’d typed my account details wrong into Monzo as I couldn’t seem to copy and paste the account details, but I logged out and back in and it showed up.

Probably not a direct participant of the FPS scheme?

First time if happened with Tesco I thought I’d done something wrong. I’ve waited up to 30 mins before now.

Good rate! I’ll check it out,

Hopefully an app follows soon.

Thanks for posting everyone.

I see it like this too, it certainly appears to be heading in that direction anyway.

It’s a fully fledged retail bank, so I’d have thought probably is a direct participant. Anyhow, here’s what their website says:

Also, on another note their Terms & Conditions are such an easy read, which is great to see.

Just added from my Monzo joint account and it took about 10 mins.

Edit - I added a second payment which went in instantly - Not sure if it’s only the first payment that is slower.

This is going to be the place I hold any savings I want easy access to now (previously it was Starling).

Annoying it doesn’t have an app - But the web interface is decent enough.

1.5% isn’t going to win any prizes, and I can see the other banks trying to compete with it soon.

But the sign up process was really slick, and the web interface is nice (looks good on mobile as well).

Edit -

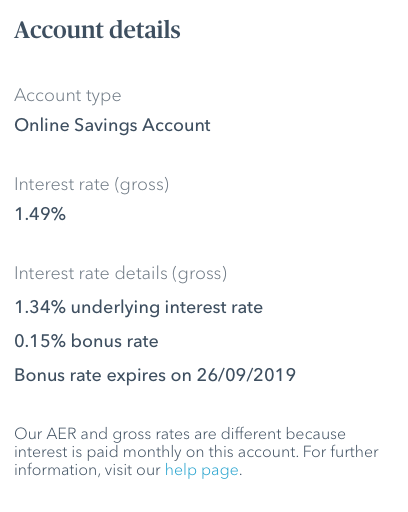

Anyone know what I’m missing? They advertise a 1.5% rate, but it’s actually 1.49% when you get into your account.

Nice to hear confirmation it works with Monzo.

Thankfully today’s FT article on this says:

Goldman plans to develop an app soon and expand into consumer lending and tax-free Individual Savings Accounts over time.

This is currently winning prizes for me because it truly is instant access with no caveats for minimum deposits or withdrawals like so many of the competitors have:

https://www.which.co.uk/news/2018/09/marcus-by-goldman-sachs-launches-in-uk-with-top-savings-rate/

This is kinda why I’ve moved my instant savings from Starling.

But the bulk of my savings are “locked away” in other accounts - So whilst it’s nice to have more than double the interest, it’s still not going to be a huge amount at the end of the year.

But… It’s better to have it than not I guess!

From their help section:

AER stands for Annual Equivalent Rate, and it’s a rate used by UK banks to help customers compare savings accounts. The AER illustrates what your interest rate (called the gross interest rate) would be, if interest was only paid and compounded once each year.

For example, if interest is paid once a year then the gross interest rate and the AER would be the same, as interest is only applied once. But if interest is paid monthly – as with our Online Savings Account – then the AER will be higher than the gross interest rate. This is because the AER will take into account the compounding interest that you earn every month over the course of a year.

By showing the rate in this way, you can confidently compare accounts whether they pay and compound interest monthly, quarterly, or yearly.