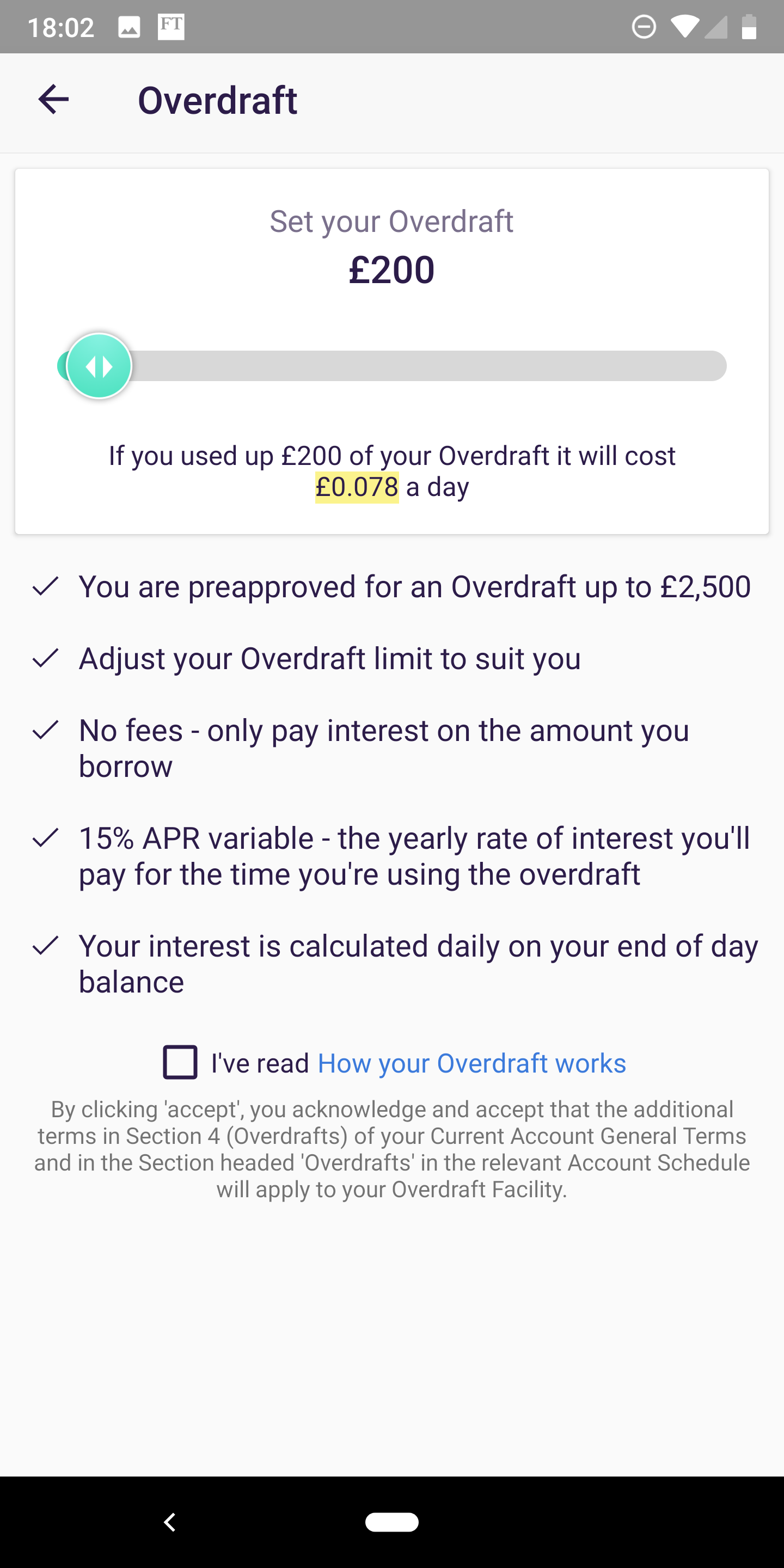

Monzo would only give me £500 and won’t increase it, so you could argue that’s detrimental to be paying 50p a day when others got double and are still only paying 50p a day.

I note the option to reduce my limit to say £50 or £100 which is laughable. No way would I reduce it to say £50 as that’s when you get very high AER/APRs

Being -£20 and having it in savings makes no material difference to me (for the majority of most months), but I keep my Monzo account OD at that level just as a point of principle.

Whether they will notice, I doubt it. But anyone that does data mining at Monzo will see my account is nearly always between -£10 to -£20 OR -£499 to -£500. I wonder how many other customers are like that.

I don’t use Monzo as my main account at all really (sadly), because the credit offerings are so poor. Keeping money in main (legacy bank) accounts to improve my internal scoring there will enable me to access better & more beneficial products, so it’s a no-brainer, as much as I like Monzo’s notifications etc.

I do completely agree with FCA rules, and like others strongly disagree with Monzo’s current pricing - although it must be remembered that legacy banks are a heck of a lot worse.

I worked in one bank where a customer was charged hundreds for persistently using her card (not knowing she was overdrawn). I got all the charges waived, but had to argue with Head Office for it to be done as it was well above my authorisation level.

Most banks have got better and introduced daily & monthly caps over the last few years, but say £50 of charges is still far too much for 90% of the population to be able to afford!

Will be interesting to see what the new cost/APR is on Monzo. A risk that OD %s will now go up a few points, as auth & unauth ODs must be the same price.

But it’ll never be anywhere near enough for the most disadvantaged of customers to continue to be as penalised as they currently are - banks would never let an unauth OD get high enough for it to be racking up say £50p/m in charges and the disadvantaged likely won’t have high enough limits (and if they do have a very high auth OD limit to keep the bank’s cash flowing, persistent debt/responsible lending/TCF then comes into play).

Risk based pricing is now my real concern - they’ll treat auth & unauth ODs at the same price, but authorise an OD of £50 @ 99.9% to a high risk customer, so that when the customer busts that they can then rack the charges up (but still not as awfully as before). Presumably, if the customer hasn’t applied for an OD they can’t then have risk based pricing applied to an unauth OD??