Yep, that first screenshot is from Chase’s Privacy Policy I believe, which is the document I read. While the links to the websites of all three CRAs are there, it doesn’t explicitly state anywhere whether they do indeed report to all three. I agree that you could make the inference that by the fact that all three links are there they do report to all three, but an actual confirmation is all I wanted! I would’ve been surprised if a newly launched bank was reporting to all three from the start, tbh.

It is interesting that the response you got is in complete contradiction to the one the user over on the MSE forum that @Seb mentioned received (shown below)

I’ve just re-read it and yes, a very sneaky way of wording it imo:

With our UK-led support team, there’s not a chatbot in sight.

I tried to find out when I would be more likely to be put through to Scotland as opposed to Asia and the guy just said that they work ‘parallel shifts.’ It was completely during the working day, UK time, for context when I chatted with them. I thought this would mean I’d be far more likely to be connected to the UK support, but apparently not.

They sent me a message asking me to call up because their email with my code had gone undelivered - strange given I got the initial ‘wait for your code’ email.

What’s stranger yet is that when I called up, I was informed that I needed to wait a bit longer due to the volume of codes at present… which makes me wonder why they bothered sending the email!

Also a little surprised that the respondent had to put me on hold to find out what to do, given that most of what they’re dealing with at the moment is surely people signing up and dealing with codes?

for context, I was just put through to someone whose English was good but definitely not native - I think it’s likely to be only escalations that go through to Scotland, or possibly when you call a different number

JPM must be throwing an absolute fortune at this, and it can’t possibly be sustainable. Whether the rewards eventually fall by the wayside, or customer services fails to keep up with growing demand, or something else, I don’t know, but there’s no way the Chase will be able to keep paying cash back on this scale whilst simultaneously having an army of customer service staff on standby to answer my questions in 30 seconds. I suppose they’re hoping that they’ll cross sell other products in future, or that we stick with them when the rewards stop (although I get the impression that rewards of some description will always be a part of the offering).

The app

I still think it’s pretty good but there is some oddness.

The map that appears with each transaction is tiny and can’t, as far as I can see, be expanded/scrolled/zoomed.

There is no running balance displayed in the activity screen / list of transactions. I guess the answer is to check the statement, but statements appear to be generated monthly, so I don’t have any yet.

I’m surprised at how much I miss the left to spend graphic that monzo have…

These little lines convey a surprising amount of information.

The numberless card

I suspect this will become standard, given that Apple have started it and Chase are following. It looks good. It means you can lose and replace your physical card without having to change your online subscriptions. What’s not to like?

Banking services

What banking services? These are very much a work in progress.

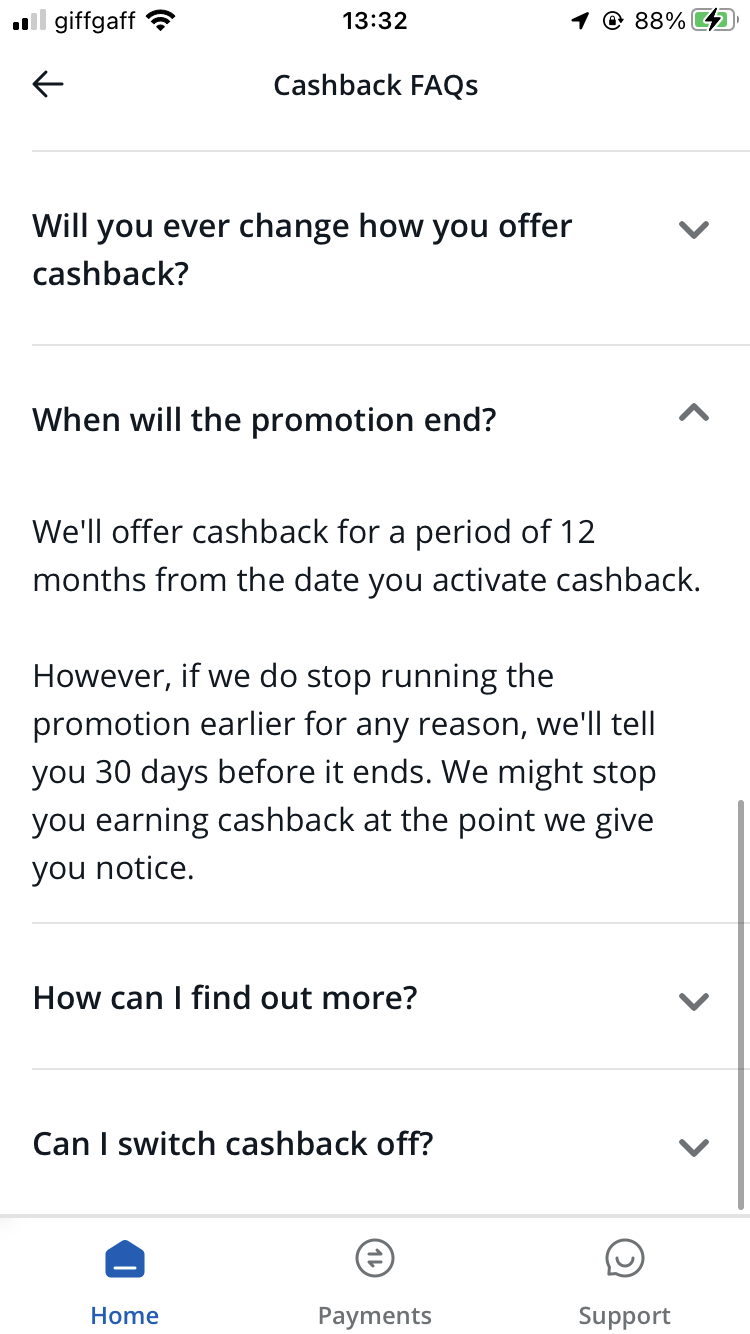

They’ve not hidden that this is for one year, the cashback. In the same way that many companies throw money to make an initial loss but they plan on making gains once customers are on board.

You could try setting a budget, though I know it’s not the same:

Applied yesterday, after a short wait asked for a picture of my passport

At that point I thought they were just checking my application to make sure it is actually me, but no, got my passport out of the safe today, uploaded it via the app, it then asked for a pic of me smiling within the circle in the app. Thought that was strange as everyone else says do not smile etc. About 10 minutes later, I got an email telling me account was now opened and asked how I wanted my name to appear like on the card, giving me a few choices and asked me to put in the PIN number I wanted for the card.

App fully working, just waiting for the card now.

Wonder if they are doing soft credit checks and initially accepting those with very high/perfect credit scores?

I think the American offer to open an account is $225 so I doubt they are short of cash, and putting this much effort and funding into it shows they may be in for the long term.

Chase said they’d been working on this for years (probably been following Starling and Monzo closely) to get an idea of what to do.

I’m guessing the direct debit thing is a regulatory problem they’ve not overcome yet but i don’t feel it’ll be too much longer as they know the UK strives for direct debit support. It’s a need, not a want.

I would’ve been surprised if a newly launched bank was reporting to all three from the start, tbh.

I would’ve been surprised if a newly launched bank was reporting to all three from the start, tbh.