A bit bored at work today, I was going to compile a list for myself of high street banks and their savings offerings, to see if there are any “proper” high street banks that offer a decent high-yield savings account. I couldn’t actually find a list of which banks are considered high street banks, so I am curious if we could collectively come up with a list? Obviously NatWest, HSBC, Lloyds, Barclays, etc… I personally wouldn’t count just any bank with a physical presence though - Metro Bank is brick-and-mortar but clearly aren’t in a very stable position.

I’ll be honest, I don’t really know the difference between a building society and a bank… (we don’t have them in the US as far as I’m aware, unless they are like credit unions?)

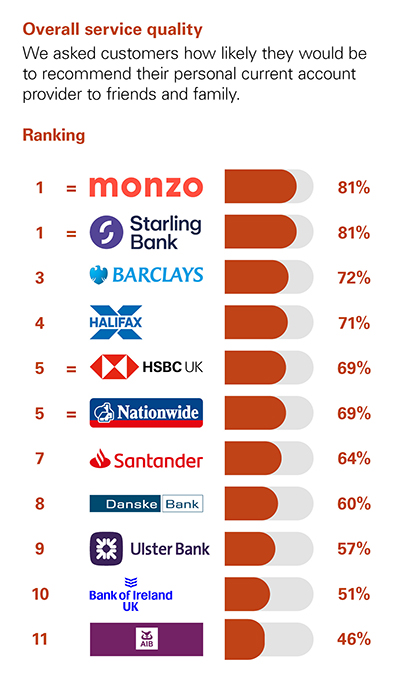

Santander

HSBC (and First Direct…)

Bank of Scotland

Yorkshire Building Society

and I’d trust any of them to be honest. YBS seems to have better rates than most of the main banks so I’ve got most of my savings with them at the moment.

I don’t know a great deal about US retail banking, but I imagine it’s a cultural difference that most UK savers would be more likely to consider a building society savings account somewhere separate from their main day-to-day banking for interest-bearing savings. Many of them are regionally-based and technologically rather basic - no apps, some accounts can only be opened in person or by post - but as a result they seem to pay higher interest rates than the banks.

The exceptions are the bank savings accounts which are only available to current account customers, but as you’ve said previously, those often have their own limitations (e.g. maximum balances or limited deposits per month).

For the record, I’ve previously used Skipton and Principality BS for higher interest rates (including when I sold a house and wasn’t buying straight away). Skipton are unusually modern, despite being a regional building society with a passable app and accounts that can generally be opened online.

Although Nationwide is technically a building society, in most respects it operates just like a retail bank and its savings rates are generally no more competitive than the banks.

Due to the FSCS, I’ll basically trust all of them.

I wouldn’t have any as my sole financial institution, but that’s more about taking advantage of different products/features at different institutions than it is about trust.

Interesting, have they had them before? Can find supporting information on their website after I search, but nothing prominent on their website about it.

Don’t think it’s ever been used in relation to a large bank failing, but I think several smaller banks failed in a short time period during the 2008 financial crisis. FCSC would have provided compensation at the time. Not sure about time scales.