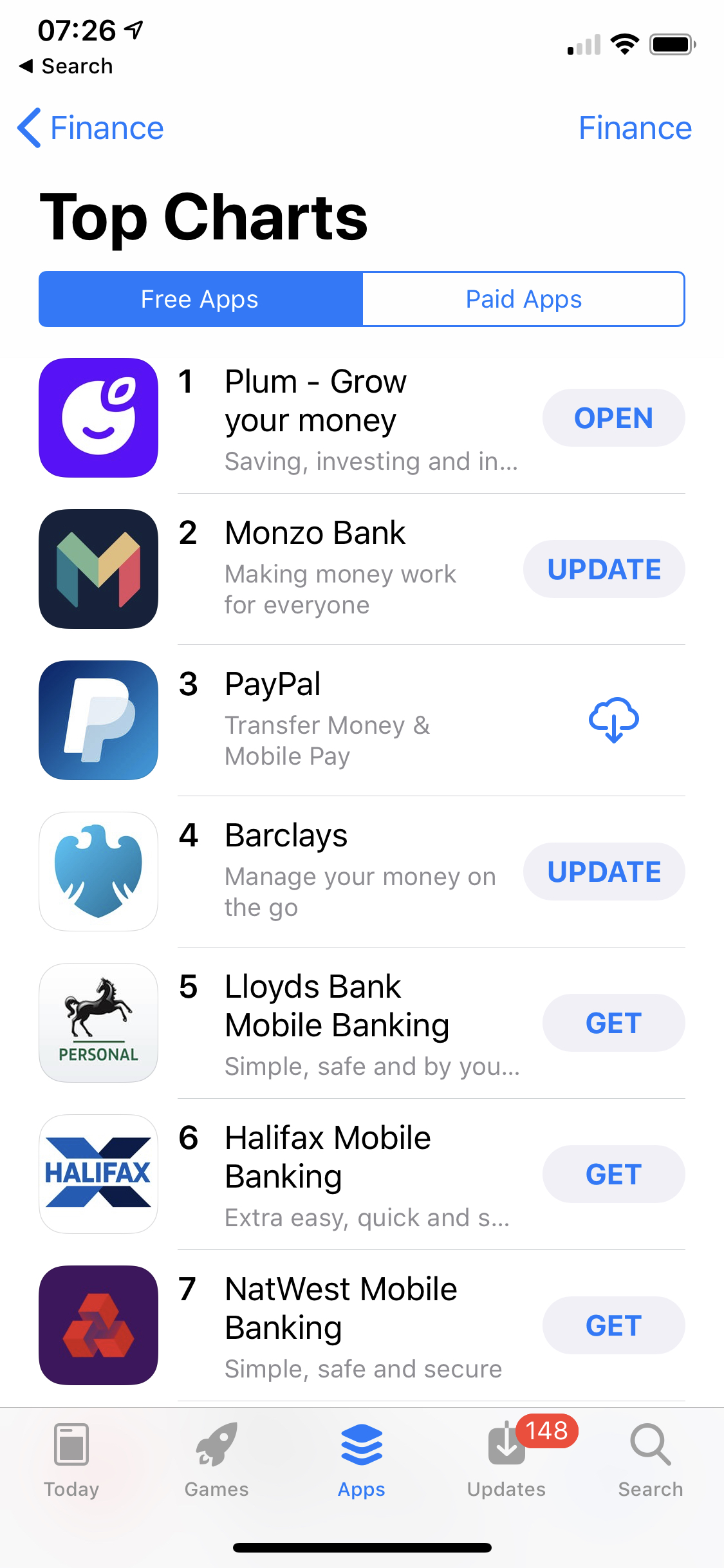

Plum briefly managed to overtake Monzo in the iOS AppStore and has maintained a top 10 ranking for a few weeks now:

Referral Wiki