Interesting stats… divorce rates go UP at retirement. A historic study showed that civil servants lived on average just five years after they retired.

You won’t know for sure what you’ll do til you hit retirement age. If the job remains interesting, minimal hassle (WFH helps that no end) and with enough flexibility to suit you, I’d say many people would work longer than they’d have expected. Different situation if you’re in a boring job, lots of hassle, etc., of course.

You don’t need to take out the non taxable bit in one go. For example, if you had £100k, you could take £12500 of it in years one and two, then from year three up to (at the moment) £12500 per year also tax-free.

I don’t think you can have a joint SIPP so that part of your plan won’t work. Max you can contribute if you’re not working is £2880 (£3600 gross).

We have a joint SIPP. I’m not sure how many firms offer them, they’re quite specialised. But as I said, although the funds are invested “as one”, they keep track of how much belongs to each of us. And they’ve already suggested the contributions in and out of the bank account as a tax- and cost-efficient way to draw down.

Don’t forget too that the state pension is taxable and will pretty much use up your tax-free allowance at current rates. I.e. any other pensions on top will be fully taxed.

But you can take the taxable element before your state pension kicks in and only pay tax above the personal allowance. From 55 in my case, 57 for my wife. And the tax free 25 percent is just that, tax free even on flexible drawdown irrespective of how much else you take.

That’s not a joint SIPP, it’s two separate SIPPs that are managed together.

I’d be asking for a second opinion as, if my understanding of what you’ve said is correct, it’s breaking tax law in a bad way.

To be clear, when you stop working then the maximum that you (or anyone else) can contribute to your SIPP is £2880. Any more and you will get hit with a 55% tax charge. It is NOT a joint SIPP as I say.

The SIPP is a wrapper for investments. It has a name, The “name” SIPP, it’s a trust with me, my wife, and the management company (Mattioli Woods) as trustees. It has both our pensions in it. As long as the contributions are correctly tracked and allocated it’s fine. It’s a joint SIPP and not breaking any laws.

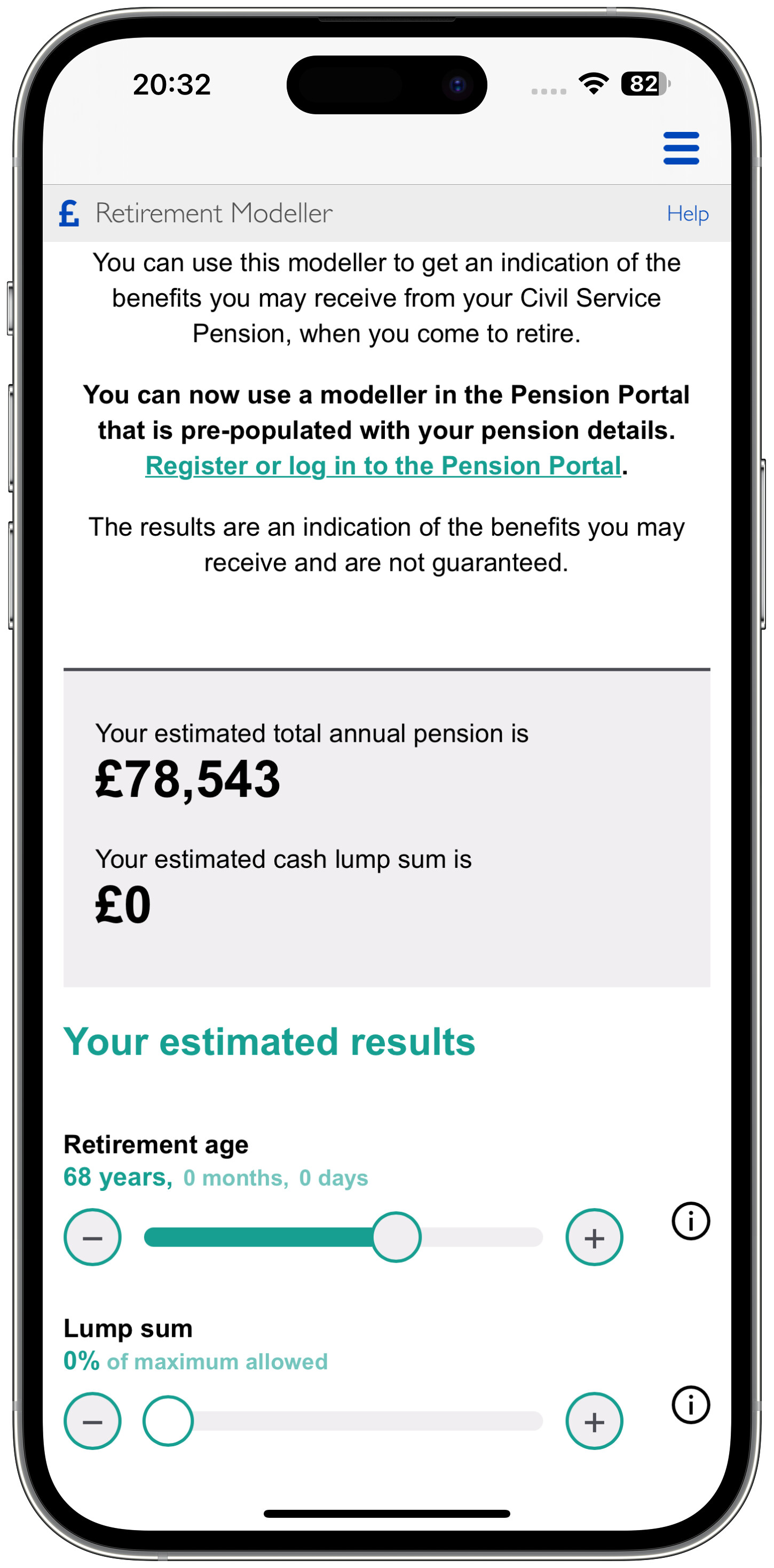

I’m already lost even with that! We have an app that I can see my pension (but only since 2020 so my previous pensions are with other providers) and I can’t seem to find my total amount so far, only what I would get currently per year if I retired and added nothing more to it (about £3.5k a year).

There’s a calculator for adjusting when I retire, and how much of a lump sum I could take (but again this is assuming my salary remains the same now and I would like to think my salary is going to increase between now and when I’m 68):

The projections they use assume fixed growth rates of, if memory serves, 3, 5 and 8%. In practical terms, these are largely meaningless.

It’s just as meaningless to use real past figures. T212 for instance tells you the real past performance of your portfolio over the last five years (to a max of 20%). Does that mean that I’ll actually get 20% return each year for the next 20 years on my portfolios? Somehow, I suspect not and equally the 22% that it’s gone up since January is unlikely to continue.

They always assume no increase in salary or contributions. What they should say is your fund will be worth X assuming a low, median or high growth rate (those being the 3, 5 and 8% I mentioned earlier).

What you can do is run up a spreadsheet and put more realistic figures in. Not that difficult really and it will likely give you a better feel of what you can expect. More importantly, it can highlight if you need to put more money in and you’ll see why the advice is always to start saving earlier.

See I’m already lost. I literally just have money go from my salary to my Civil Service pension and that’s it. What I get at the end isn’t going to be an exact science but generally it’s a good amount and everyone in my team who retires either does so a good 10 years early or has a £150k+ lump sum at normal age

I’m as I’ve said I’m putting in 4.5% and my employer 29.5%; from what I know I don’t think I need to add much more myself.

I contributed a very small amount into a pension when I was 21-23, and then I switched jobs and didn’t contribute anything for about 4 years.

Then at 27 I got a new job and started contributing straight away, and have been contributing ever since, maxing out the employer/employee contribution.

It’s definitely worth it in the long run, especially if you’re a higher/additional rate taxpayer.