Not officially, but I believe you can do this via IFTTT

From a standard pot, yes, but you can pay Flex directly from a pot anyway.

Savings pots can’t have any scheduled withdrawals as that defeats the point of “saving”.

Someone else has mentioned IFTTT which can be used with Savings pots but uses a 3rd party service (IFTTT) rather than Monzo directly.

1 Like

Hey folks,

Sharing a quick update on the Flex Build pilot. Let’s get the legal bits covered first:

- Not everyone will be eligible for Flex. We will run a soft credit search to assess if you’re eligible, and a hard search if you open Flex.

- As a minimum, you’ll have to be over 18 and a UK resident, and you’ll need a Monzo current account to apply.

- Flex Build representative example: 39% APR representative (variable). £350 credit limit. 39% yearly interest (variable).

- If you miss a payment this may negatively impact your credit score, and you won’t be able to unlock some of the additional features like limit increases. Ts&Cs apply.

When speaking to Monzo users about the initial Flex Build pilot early last year, lots of people told us they were finding it hard to access credit cards - especially if they’re new to credit in the UK or have missed payments in the past. So we’ve been working on expanding who we can offer Flex Build to.

This week we’ve started piloting a version of Flex Build with a deposit, which will allow eligible customers that haven’t used credit before or are repairing their credit file to open Flex Build if they put down a deposit first. Here’s what you need to know:

- If you’re eligible for Flex Build with a deposit, we’ll ask for a deposit that’s either 25% or 50% of your starting credit limit. So if you choose a starting credit limit of £250 we’ll need a deposit of up to £125. You can choose a smaller starting credit limit so you can get started with a smaller deposit, as low as £12.50.

- The deposit acts as a “security”, which means we’ll set it aside and you’ll only be able to access it in a few situations like to catch up with a missed payment or when you close your account.

- We’ll give you back your deposit in as little as 6 months, as long as you keep on track with your monthly Flex payments and other borrowing / bills you have.

- Other than the deposit, everything else works exactly the same as Flex Build without a deposit.

We’re testing this with a very small number of users until later this year, before we decide to roll it out more widely. So it might be a while until you hear any more updates.

Tom

35 Likes

Interesting. So your lowest Flex limit is £25?

I get the credit building side to things, but I can’t help but feel someone needing to pay £25 in installments shouldn’t be doing so!

4 Likes

For this version of Flex we offer starting credit limits of between £50 and £350. Customers can increase their credit limits within the first 3 months if they keep up with their repayments, so that starting credit limit can grow quite quickly.

Credit builder cards aren’t necessarily about paying in instalments. For many people we spoke to it’s having the opportunity to build a credit record and demonstrate they can make on-time payments. For example, users can choose to Pay in Full and put one small shop on their credit card a month which they pay in full. That’ll start appearing on their credit record as making regular on-time payments, and hopefully they’ll start to see their score increase over time.

16 Likes

It did seemingly only be new customers, don’t think they ever said it wouldn’t come to current customers.

1 Like

I opened Flex a few months back and I can only flex purchases of £100+. I did it a few times but tbh I like to clear out everything at the end of the month anyway so it was pointless for me. I’ve ended up going back to my NatWest credit card for daily spending anyway though for other reasons.

2 Likes

I am thinking that using “flex” as a verb may be confusing.

If by “flexing” a transaction you mean pay it in installments, then yes, only >£100 transactions can be flexed.

But if by “flex” you mean use your Flex card to pay for something, this can be done for any amount. It’s only installments that can’t be done for less than £100 value.

I don’t think anyone has been confused so far.

10 Likes

I added my Flex card to the Wallet app on my Mac yesterday. Today I’ve received a text from Monzo saying that I started adding my card but didn’t finish and what to do next. Thing is, though, I did finish and it works fine.

Obviously it didn’t register the success at Monzo’s end, even though it’s all working properly.

I got the same when adding my card to my iPhone, last year, I just ignored it.

Yes, that’s what I’m doing since everything is working.

How many texts did you get and what did you do to stop them?

I’ll see what happens. I had the same with my RBS debit card but their texts stopped after (I think) 7 days.

If you DM me your email address we can take a look at what’s happening ![]()

1 Like

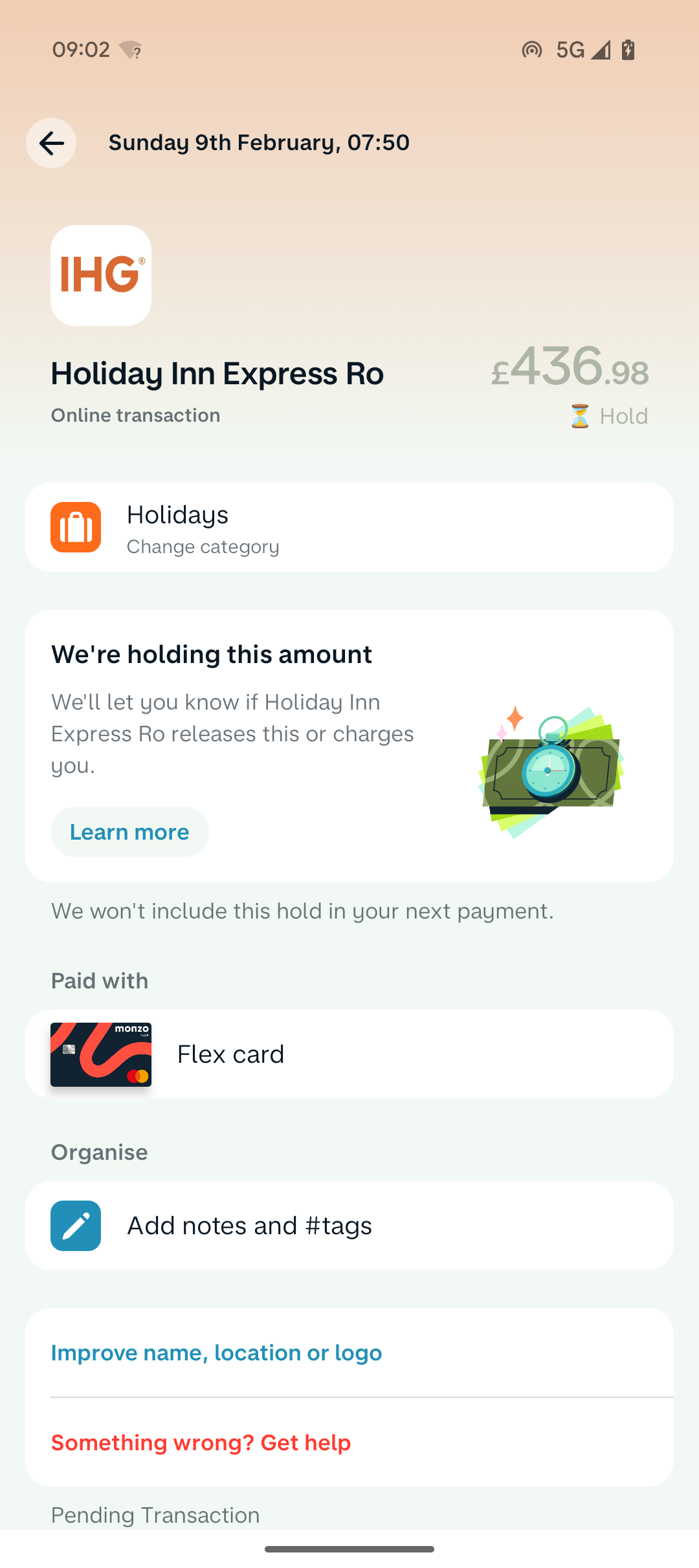

Just wanted to say I’ve not noticed how Flex handles hotel holds before as I can’t recall using it to pay for one. I recently booked a holiday Inn express using flex (to take advantage of a Monzo cashback offer) and have to say I’m impressed with the clarity from Monzo about the hold, how it works (really nice clear explanation when clicking learn more) bravo

24 Likes

I recognised the logo as IHG is loyalty program for holiday Inn (and a number of others) and is also who the cashback offer was for.

1 Like

The logo would be correct. If you spent this inside the hotel I would assume it shows the Holiday Inn logo.

1 Like

This is really cool tbf

1 Like

It does clearly explain on the second screen after clicking the button that as it’s a hold it won’t be included in my next cycle of flex charges and neither will I be charged interest but the available funds are on ‘hold’.

The hold has actually been charged now so I can’t share a screenshot of the wording but it actually gives me more visibility of what’s going on compared to my MBNA card, or Barclaycard.

11 Likes