Yes, let’s not loop. Some new points though, if you are interested:

Regarding this:

Mortgage availability to FTBs is a factor, yes, but not the only one as FTBs don’t dominate the market. Movers, investors (foreign, domestic, BTL), are all in the mix, too. More importantly, the largest contribution is from interest rates, which the Bank of England now freely admits:

house prices relative to incomes between 1985 and 2018 can be more than accounted for by the substantial decline in the real risk‑free interest rate observed over the period

This is, sadly, a pernicious myth. It’s promulgated by just about every media outlet, and the government, because it neatly sidesteps the affordability issue, both absolving (and, importantly, reassuring!) homeowners. There are multiple aspects here; the historical house price building rates don’t take account of new building - much in the 50s and 60s was post-war rebuilding, the government’s statistics about projected household growth has been revised down each and every year, and building more would not, at any rate, cause much appreciable change to prices. Have a look here for some more info.

I know that these are all bitter pills to swallow, but understanding them is better than parroting the deeply flawed status quo.

But it’s been a “risk” since day dot. It’s always a warning from everyone and if it does happen, it will hurt millions but it always seems to be “coming”

So I’ll come back to say, I have had a look there but not really learned much new. The article is confused and poorly written, and then goes on to cite a load of sources that don’t support his conclusion in a classic ‘let’s make ourselves look like we know what we are talking about and hopes no one checks’ approach.

Unsurprisingly, there is no ‘overwhelming consensus’ among economists that building houses won’t affect affordability. Or actually, about anything else, at all, ever

Btw for the models, I think by and large what they show is that 300,000 a year just isn’t enough houses

A talented & successful knowledgeable finance writer could bring out a 1-3 page write-up and really bring a new light on owning uk property.

Much of the country needs to think more globally when it comes to income and to understand that the uk only makes up around 4% of the global economy.

We are clearly at a point where a huge amount of the uk population can not make sense of a single salary or even a couples salary to purchase a home. A talented financial writer should be able to produce a new mindset on how to create more than one income per person in order to afford a uk property.

An incredible amount of uk homebuyers pretty much sacrifice life for 20-30 years due to the mortgage.

Gen Z especially and millennials should be using a different mindset to not just get on the housing market but to boss their own life.

I’d love to see a small bunch of awesome finance & property experts piece together an actionable write-up covering this. Like, real actionable stuff.

Wages are not going to increase the way the dreamers think and property is never going to be cheap over here. A new mindset and combined skill set is needed. The younger generations should not hustle eachother to get ahead like the previous generations, new mindset and direction needed.

It’s a highly sought after area, the kind of “end goal” place to live and style of house to own. Why should prices be reduced to be more affordable for a first time buyer?

Do as I did. Buy a cheap tiny house in a small town somewhere (yes I had to move away from mummy and daddy), usually in a slightly dodgy area too. Build equity and climb the ladder. If you really want to live there one day, it’s certainly achievable.

I feel bad for them to a certain extent because it is hard.

Its a hard reality check when you become and adult and your carefree days are behind you. When it hits that you can’t have everything you want, things certainly aren’t fair and you will have to make lots of sacrifices - it’s horrible.

To put it bluntly you have two choices. Stomp your feet and get nowhere or roll up your sleeves and do something about it.

It would undermine everything the current occupants put in if prices were to crash to such a low level and it makes me wonder if they’ve even thought of their potential neighbours and the impact it would have on them. They certainly wouldn’t be welcomed to the community

Rural and remote working is difficult believe me. I’ve moaned plenty about broadband , phone signal is bad and it’s expensive if you aren’t connected to gas or sewage lines too.

They’re all things I learned since buying the house we’re in now.

Yeah you’re definitely lucky on the broadband front My only option is 4G and I have zero signal so need to use WiFi calling. Which as you said is tricky when there are outages.

All solar grants appear to have ended a while back too so we’re stuck with LPG for heating and hot water.

The biggest one is that I only have a few takeaways that will deliver here and they’re all terrible Along with very few delivery drivers being able to find the property.

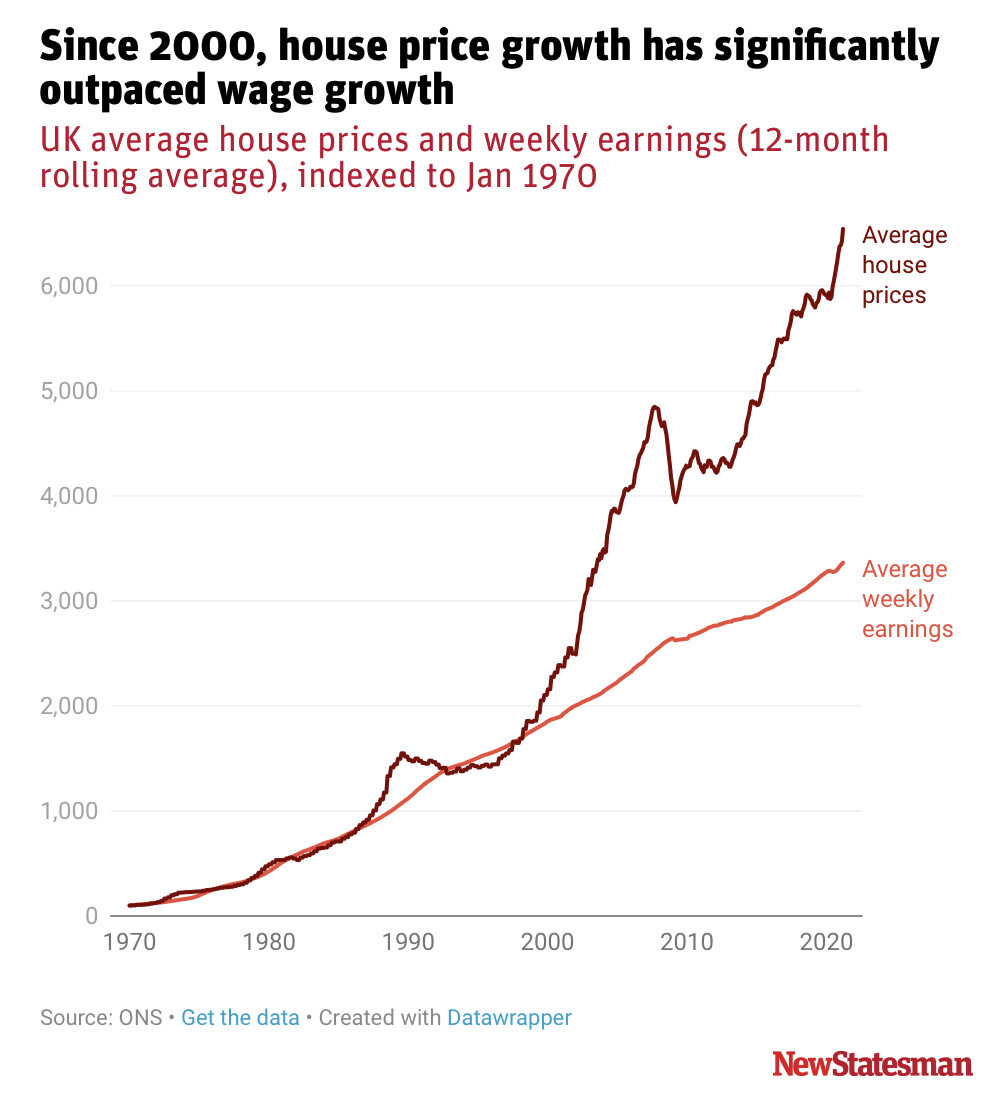

It seems a bit disingenuous to pretend that, just because you did it a few years ago, other first time buyers can do it now when this is what’s been happening to house prices vs wages:

This misses the point. If it’s a bubble, it’s better to correct it sooner rather than later. Stamp duty cuts, help to buy, 95% mortgages, etc are unlikely to be a long term solution.

My parents bought my house (south east) in 1993 ish for 42k, when their combined income was around 11/12k. So it was roughly 4x their income and they only cared about my dad’s income back then.

If I wanted to buy this house from them it’s now worth 280k. So on my income 42k it’s roughly 7x my income. Bank won’t lend you anywhere near that, so it would be impossible to buy.

I could as you suggest, look to move further north and buy a house in a not so nice area etc (personally I could afford to do that) but why shouldn’t I be able to buy in the town I grew up in?

If you’re single like me, it’s very easy to get priced out of houses very quick.

I’d personally be 100% in favour of a correction in house prices (maybe not a huge crash). Houses should be homes, they shouldn’t be assets.

I was in a similar situation. No way could I afford to buy the house I lived in (that my parents bought for 80k ten years prior!) so I bought a flat instead, because that’s what I could afford by myself.

I didn’t get a house and I had to move to a different area a few miles away. But I am now on the ladder.

Yes I’d ideally like a house. Just because I’m single doesn’t mean I shouldn’t be able to afford one. For sure, I shouldn’t be able to buy a 3/4 bedroom home but I definitely shouldn’t be priced out of a 1/2 bedroom home.

In 1993 base interest rates were about 6%, making borrowing rates about 7-8%. Assuming a 25% deposit, borrowing 30k at 7% would mean repayments of £212 / month.

If you were to borrow 70k today for an 80k house (to keep the deposit consistent) you’d probably be getting an interest rate of about 1.5 - 2%. With 30 year deals now widely available (they didn’t used to be), you could well end up paying about the same or a bit more than the first scenario - somewhere in the range of £215-£250 a month. You also wouldn’t be paying stamp duty and you’d have help to buy schemes available.

I do get that actually borrowing more than your salary is the hard bit. I had to work 7 day weeks & 2 jobs for a year or so in order to ‘inflate’ my annual salary figure in order to borrow what I needed, but a bit of overtime for a couple of years doesn’t hurt that much. In terms of affordability when you do get on the ladder though, despite the salary multiples it really does work out quite similar to how it was in the 90s.

There is no denying that prices have gone up but I was referring to the article and their crazy demands.

That being said is it essential to own a property? I couldn’t afford one until I graduated and saved for many years, so I rented and there’s nothing wrong with that.

I generally think the article is about very specific places.

I do agree with some people in the article that there is a problem in places like some towns in Cornwall with local communities being priced out by second home owners. But this probably applies to <1% of the UK population and is best solved by reserved housing schemes in those areas. Clearly a nationwide house price crash isn’t really a good solution to that.

, phone signal is bad and it’s expensive if you aren’t connected to gas or sewage lines too.

, phone signal is bad and it’s expensive if you aren’t connected to gas or sewage lines too. My only option is 4G and I have zero signal so need to use WiFi calling. Which as you said is tricky when there are outages.

My only option is 4G and I have zero signal so need to use WiFi calling. Which as you said is tricky when there are outages. Along with very few delivery drivers being able to find the property.

Along with very few delivery drivers being able to find the property.