The reality is that the vast majority of investors don’t have the time or inclination to get into the market mechanics. For that class of investors, I believe they’re better off paying for a service (e.g. Roboadvisor, IFA etc.) that will create friction when they want to bail out at the worst possible time and create encouragement to invest when things look uncertain/good value.

Much more wealth is lost from individual retail investors buying/selling at the most inopportune time than paying investment management fees. That said, the cheaper the fee, the better.

If you’re a sophisticated investor who will be taking the time to stay on top of market news and can resist the urge to act, platforms like Freetrade are a good option.

I think it’s also worth pointing out that many of the people commenting on this thread are Freetrade investors. To be entirely cynical, while it is a good option, there are some inherent conflicts that aren’t being disclosed!

I use Nutmeg to manage my LISA - their fees from what I can tell are fairly low and when you think about the 25% bonus you gain with your deposits (max gained £1,000 in a tax year) it is just skimming off that bonus all in all.

The reason I use Nutmeg and have a “managed” LISA is because simply I don’t know enough about the market to dump that sort of money (house deposit) into my own decisions. At least with a managed portfolio some of the responsibility is removed.

I will dabble in Freetrade and create my own portfolio over time but will likely keep it to a modest amount of money in.

I use a mix. I have a Moneyfarm SIPP for my old accounts (they gave me a discount way back when they first launched it otherwise I was going to go for PensionBee.)

For my ISA that is with AJ Bell (was with ii but I am not a fan of the new setup.)

For my GIA I’ve had that in a few places, I do much less in the GIA now as that was more for the thrill, go big or go home kinda stuff that wouldn’t matter too much. I had that with SharePrice before, it’s technically with AJ Bell now but I don’t have the time for it.

I use Genuine Impact for my screening and research, I was using Simple Wall St before.

For Graphing I like ii’s new graphs but they aren’t as detailed as I’d like, I was paying for a service from VectorVest but again this was more for my GIA swing trades which I’m not into these days.

I’ve had accounts with Nutmeg, HL, Charles Stanley, and a few others but I found the costs off putting for what I wanted to do at the time.

I find LangCat is an excellent resource for price comparison of the brokers. I’ve been keeping my eye on Freetrade but it feels limited for now but we’ll see what happens.

Personally I use the Hargreaves & Lansdown app. It’s straight forward, but admittedly does nothing special. However the advantages comes in the fund discounts that HL offer on selected funds. Would highly recommend it as a starting point into the world of funds.

Completely agree and same experience. My funds are doing great, but the share choices…not so much…I figure that it’s literally someone’s job to ensure a fund runs well, and I don’t have the expertise or time to make the right decisions with shares.

Also, some of the funds have little to no costs on H&L, so for that reason alone, it’s a great platform to use.

What friction do the robo advisors present? I’m honestly not aware they do anything to stop you selling during a downturn.

Paying an IFA when your holdings are worth less than £5m is a distinctly foolish way of wasting money. If someone is making that kind of a bad decision, and the IFA let them, is there any reason to believe the IFA would give them good advice during a down turn, and that the person would follow it?

You absolutely do not need to be a “sophisticated investor” (in the legal sense), nor stay on top of market news. You just need to understand the basics of how the stock market works. You can acquire this knowledge by reading a good book on the subject.

Armed with this easy to acquire and easy to implement knowledge, you can use Freetrade or any other investment platform to start building your wealth.

Admittedly many people on the Freetrade forum do try and pick their own stocks, and are undoubtedly making bad choices. Many have been bitten by Debenhams, for example. But you don’t have to be that person. You can choose to invest wisely, and don’t need to pay someone to make worse decisions on your behalf.

In some scenarios it’s true their fund discounts could make them cheaper than other platforms. But generally speaking, that 0.45% platform fee is going to bite you, and bite you hard.

My view is that you should decide on your long term investment strategy, and then run the numbers to see which platform will let you follow that strategy the cheapest. None of the platforms really offer anything so compelling that you’d use them in spite of their fees. It’s just the same features with a different interface and fee structure. (The notable exception being Freetrade, with it’s current lack of basic features… but at least it’s free!)

If your strategy is “invest in funds managed by the latest fund manager that actually has no skill, but happens to have the highest performing fund right now due to luck and survivorship bias”, HL might turn out to be the platform for you.

Ribbing aside, the one place where I believe HL are actually the best in the market and you’d want to use them as part of a sane, safe and effective investment strategy, is for buying and holding UK Gilts.

I don’t know that Fundsmith and Lindsell are exceptions. How have they done during major recessions? Oh, right, they haven’t been out that long. All of their funds do really well, right? Oh, sorry, no, they do not. What happens in the future when some of the very few companies they are invested in go bankrupt? Oh, woops, neither you nor they have the ability to see in to the future.

It’s always tempting to chase high returns, but investing in a fund when it has already made those returns means you are unlikely to see those returns yourself. You might though, but this is a big gamble. Some people have that kind of risk appetite, fair enough. As long as you understand the risk you are taking.

Warren Buffet beats those UK funds in to a cocked hat. And Buffet’s advice is to invest in to a broad market tracking ETF (his suggestion being the S&P 500).

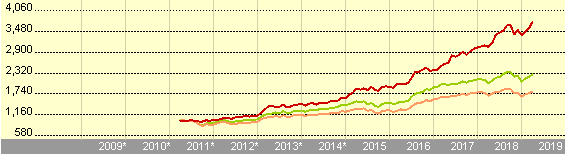

Lindsell Train Equity Fund has been running since 2011 and is an exception to the rule that a tracker fund is the best fund to follow. Argue as much as you want, but year on year, it has done exceptionally well, even when markets have not:

While I agree that a tracker fund is the right choice 99% of the time, Lindsell Train Equity is one fund not to be shy on, and Fundsmith Equity I is looking to go the same way.

My SIPP is with Hargreaves Lansdown. Fully recommended, despite the fees. I’ll strongly consider switching to the Vanguard SIPP when they ship it though, mainly for cost reasons. I also want to be more conservative with my SIPP: I constantly fight the urge to stock pick more.

Which is what they said last year, and the year before, and the year before…

Reality is, there is no reason they would logically tank, other than people emotionally holding onto the concept that a tracker fund has to be the best performing fund, because that’s what they’ve been told.

That’s exactly what I would recommend to friends/family who ask about this stuff. Just keep buying the Vanguard LS or FTSE Global All Cap every month for as long as you can. Don’t sign in, don’t look at the price, just keep buying. Saving on cost and not bottling it when times go bad is when the real money is made (for most people!).

What stops someone checking their Vanguard account every five minutes? Website or app, I don’t think it makes any difference. As a poster above put it, probably people will check frequently to start with simply because it’s new and interesting, but eventually it turns out investing is boring, and you’ll check it once per year. Freetrade, Vanguard, it’s all the same.

8 years is not a long time. Would you have picked Lindsell in 2011? In 2012? In 2013? Was there a better performing fund in 2013? One that also had lasted 8 years to that point? Where is that fund now?

Hindsight makes things look great, but you must realise that of the thousands of blind monkey managers out there randomly picking stocks, one of them is bound to beat the market on average for an 8 year stretch.

You also must understand that the performance of this fund is due its concentration. You are taking a risk to chase these rewards. Again, nothing wrong with having a high risk appetite, but the brass-balled investor willing to gamble everything is the one who invested in 2011. They are the ones that have enjoyed those impressive cumulative returns since then.

That said, as long as it’s constituent companies (and just 10 make up 60+% of the fund) continue to grow as expected, new investors may also beat the market. But betting your money on the performance of 10 companies is a risk you better understand.

Worse, these funds are managed by people who are getting quite old. Now you’re making a bet on the lives of 1 or 2 people. Another risk to understand.

But that’s the way the stock market works: for increased risk you should get a higher reward. But in my view the market itself returns plenty of reward without having to take on any non-systematic risk.

I think Freetrade 100%. If you are unsure then research what goes into the ‘robo adviser’ portfolios (Nutmeg, Wealthify etc).

You can build a well diversified portfolio easily using ETFs (the same investments that Nutmeg and the like use) but avoid paying the 0.7% pa fee very easily. In addition there are lots of Investment Trusts if you want to trust a managed portfolio instead, again without any additional fees (Investment Trusts have fees built in you need to pay, but nothing from Freetrade, you would have to pay extra on Hargreaves Lansdown for example).

If you want to hold individual stocks it is also great. Again if you are unsure, use Freetrade’s forum, and start perhaps investing in companies you use day to day - do you have an iPhone or an android phone, where do you buy your groceries etc.

I can’t recommend it highly enough, they will only get better over time too!