I think there’s a really interesting conversation to be had here - not about why Monzo freezes an account, but in the aftercare from what’s presumably a false positive and the comparison to what happens with legacy banks. It’s interesting that, in this example, HSBC contacted @HarryBarry immediately to confirm it was a genuine transaction, but Monzo left it for a while longer.

Taking everything here at face value, it’s important for Monzo to hear this sort of feedback. So let’s not make this personal. And remember that Monzo staff can’t discuss individual cases or the details of their counter-fraud measures on here.

(I suppose that’s another way of saying I really don’t want to have to lock this thread )

There’s a bit more to it than that. The whole experience was a shambles. The other nonsense isn’t actually nonsense - Monzo might not freeze more accounts, but they get more complaints about being frozen - because all other banks have a process for sorting it immediately. Monzo don’t and people vent on social media. I actually did research this on twitter before posting it, the other banks rarely get this complaint. I’ve mentioned in other posts what made me target this blog to reply to.

Exactly. The whole experience with Monzo was a shambles. For trying to make a genuine payment to my own bank (an everyday scenario that we all do) I got treated the same way an international terrorist would!

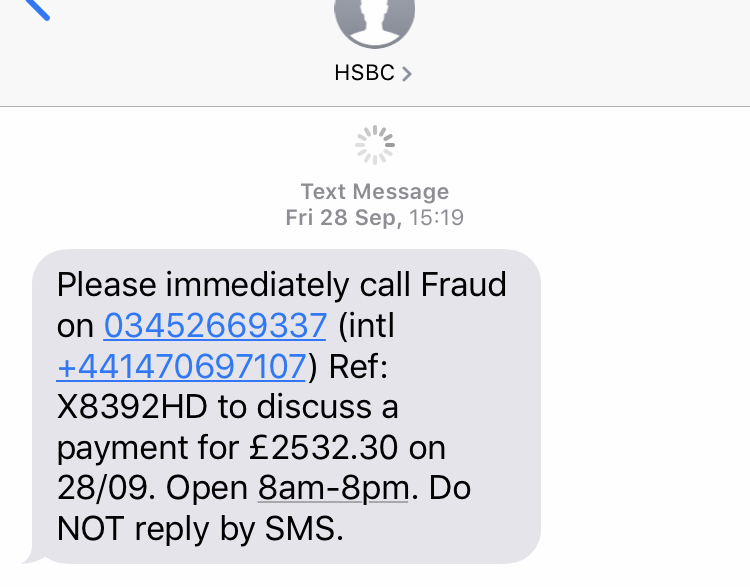

I’m attaching a screenshot of the sms that hsbc sent when it happened there, just to prove I’m not making up having experience of this same issue elsewhere.

I used to get these from Lloyds too. They’d temporarily freeze the account, but text me with a number to call.

As soon as I confirmed it was me making the transaction along with a few security details, everything was back to normal.

Edited to add: It would be great if Monzo introduced a similar process to verify flagged activity.

A payment that a bank thinks is someone else using your card details. Temporarily block the transaction, text etc, then once its confirmed it is an intended transaction allow it to go through.

The bank thinking that the entire account is being deliberately used to commit fruad/illegal activity. Then they must block the entire account and cannot legally go into more detail until it is resolved.

The problem is, and Monzo should be clear about this, they are developing fraud controls based on transactions and the data they have. Yes there is industry data, but each bank develops its own controls as fraud can vary dependent on the type of account, people targeted and so on. As a new bank it still has no where near the data of the bigger banks, so it can’t get it as right. The rules and regulations state the minimum requirements, but how the bank sees and interprets the data to report fraud is different in every single bank.

The big banks still get don’t always get it right with transaction data from trillions of transactions.

Sorry I agree that I really didn’t make that clear.

I’m aware of the KYC requirements but Monzo advertises the fact that you can sign-up minutes (just look at the app store listing).

Some old banks, e.g. Nationwide required me to, make you go in and provide ID in person. This is certainly not as convenient as the Monzo sign-up flow.

We had a similar issue with Cap One and the bank is HSBC, we transferred d £1200 by SO from our joint Monzo account that we normally clear bathe balance by DD, even with faster payments Cap One took about 5hrs to add the funds and clear them, then although we could access the account we couldn’t make a payment, just stated declined and contact issuer, 12hrs later get txt saying security checks were being completed, apologies and to now try again.

)

)