Just got an email from Monzo, saying that I can “cushion” my account with an overdraft.

I don’t think I like this. I know the lending criteria is quite strict, so I followed it through to see and they will offer me £1000 at 19% (Or similar) but I don’t like that this has been pushed on me.

I say this not to brag, but provide some context, I have more in my savings pot (only just) than the amount they’ve offered me. Maybe if I had no money they wouldn’t have emailed me, but I’m not sure if that makes it better or worse.

Also, if they can do this with overdrafts, why isn’t this inbuilt for normal accounts?

First time I signed up for Monzo, they offered me a £1000 overdraft and when I said no the wording was something like ‘risk bounced payments’ - found that to be a bit cheap & nasty at the time, tbh

2 Likes

Anarchist

(Press ‘Help’ search ‘Contact us’ or email help@monzo.com or call 0800 802 1281)

3

Sounds like they are saying “We can see you don’t need to borrow any money from us, but we can help you get into debt if it helps.”

I can’t think of a situation where they need to email me promoting it if I’m honest.

If I had £0.08 at the end of each month and I have payments bouncing, I’d certainly want one, but is it a good idea to email me about it? Could they get in touch to talk to me and see if there’s a way they can help?

I’m sensible enough (now, probably not when I was younger!) to turn it down but lots of people won’t be and especially with people taking big hits in the last year, someone might take that cushion a bit too literally.

By all means advertise or promote your overdraft. But don’t encourage people to take or push it onto them and make them feel like they need it. That’s another miss-selling scandal just waiting to happen.

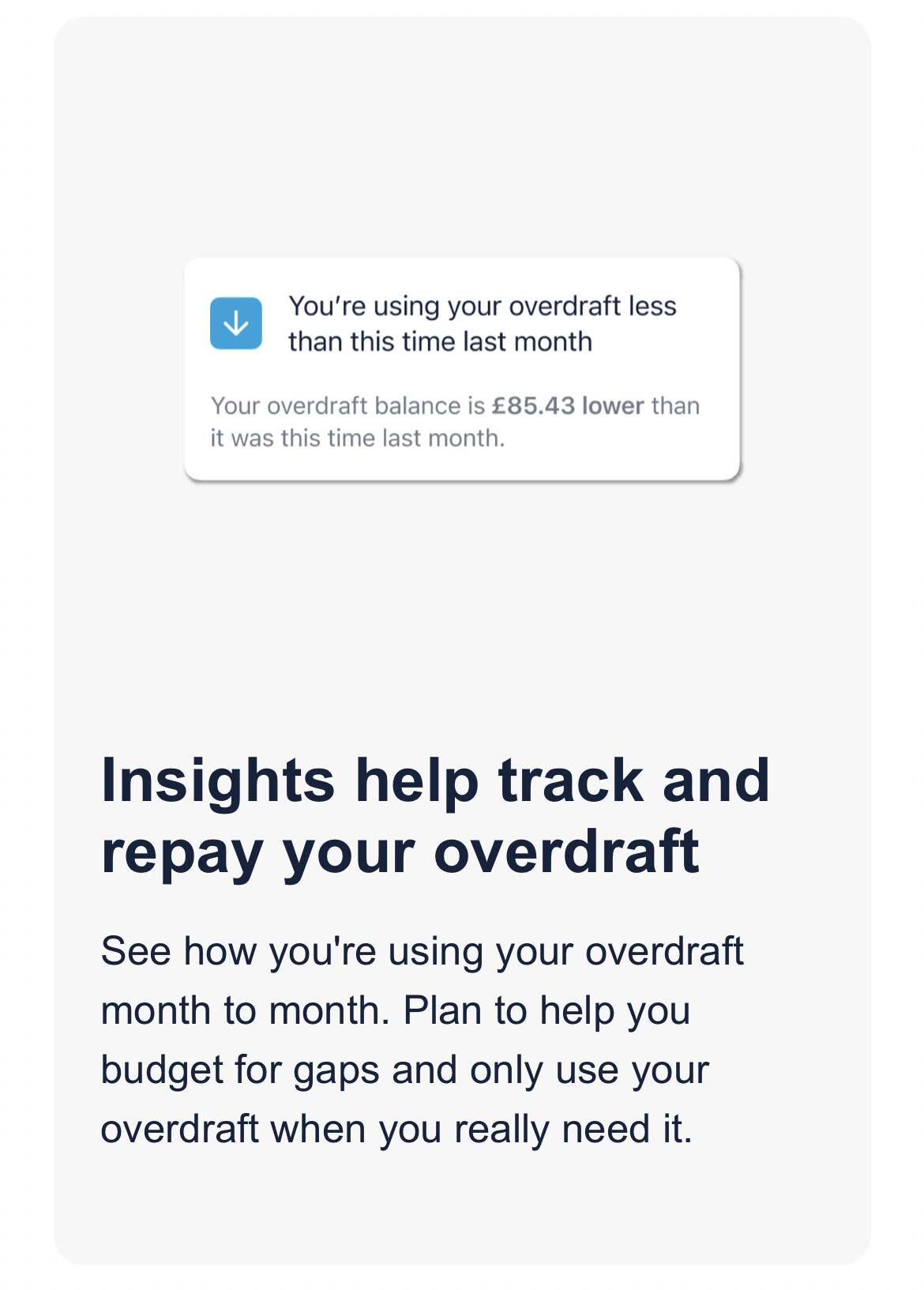

That email looks like it’s encouraging responsible use of overdrafts. It is congratulating the user on using their overdraft less and suggesting they plan so they only use it when they absolutely need to.

What am I missing?

Edit: my message crossed with the previous one. So the OP didn’t have an overdraft? Now I get it, but it all seems fairly responsible still.

and indeed helps you plan more doesn’t it … your £85 lower than last month , short of well done its great …your overdraft usage is coming down because you are planning

Sounds like these emails are targeting customers that demonstrate healthy money habits and have sufficient income. So at least, if they are pushing it on people, it’s not those who are financially vulnerable.